The Growth Curve #002

Portfolio Update, Lowe's Earnings, American Tower & Datadog Investor Conferences.

Welcome to The Growth Curve. My last deep dive was “CNX Resources: The Most Aggressive Buyback Plan I Have Ever Seen”. My next deep dive will be sent to subscribers on Tuesday, May 30th. We’re diving into Perimeter Solutions (PRM), a $1B company that provides fire safety equipment and oil additives. This link will always have the updated Growth Curve portfolio and all my transactions.

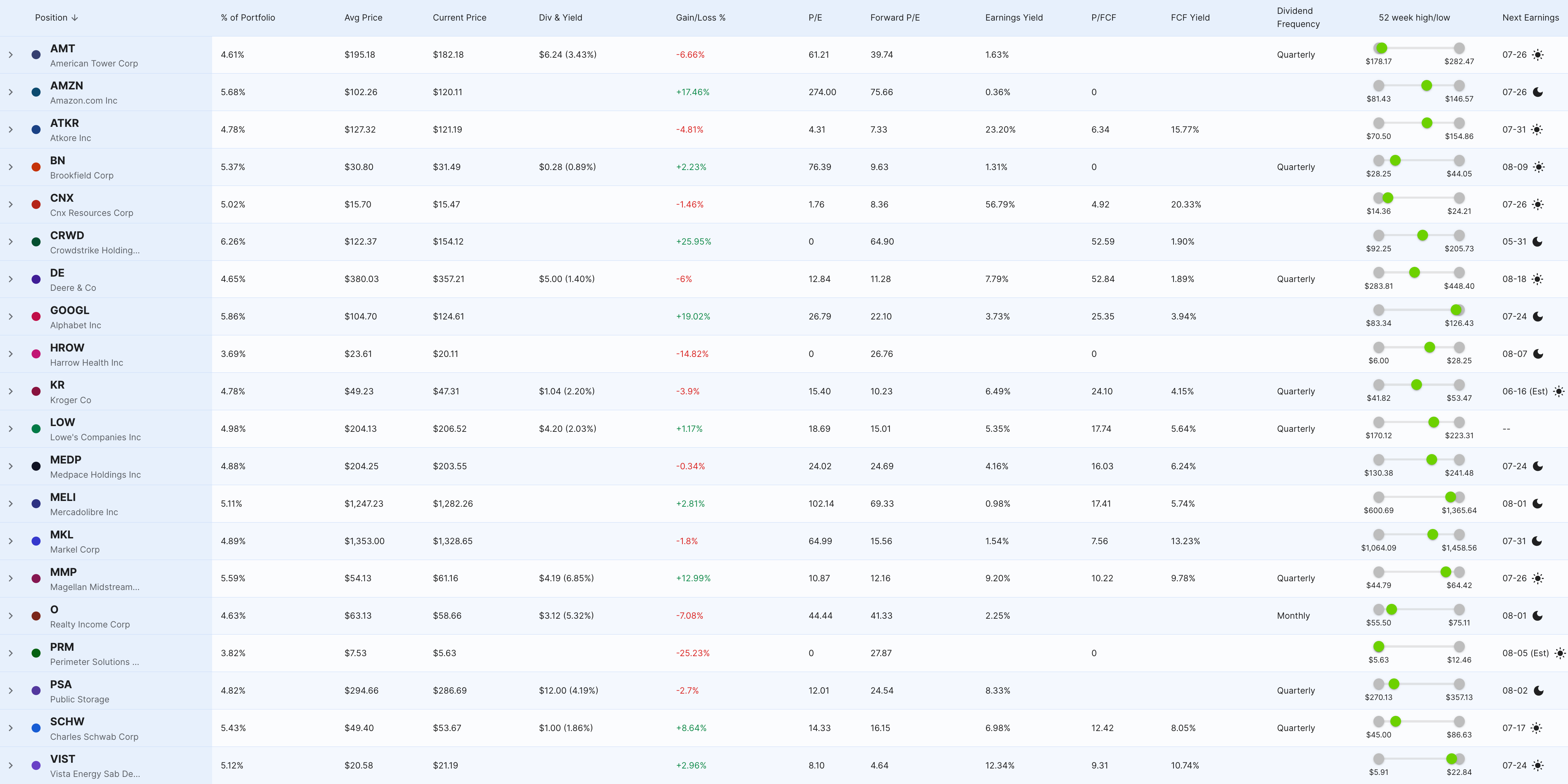

Current Portfolio

On May 5th, I switched over to tracking my portfolio using Stock Unlock because it’s way better for sharing (see below). At that time, the portfolio value was roughly $134,000, and I was up 17% YTD and down 7% since I started the portfolio on February 15th, 2022.

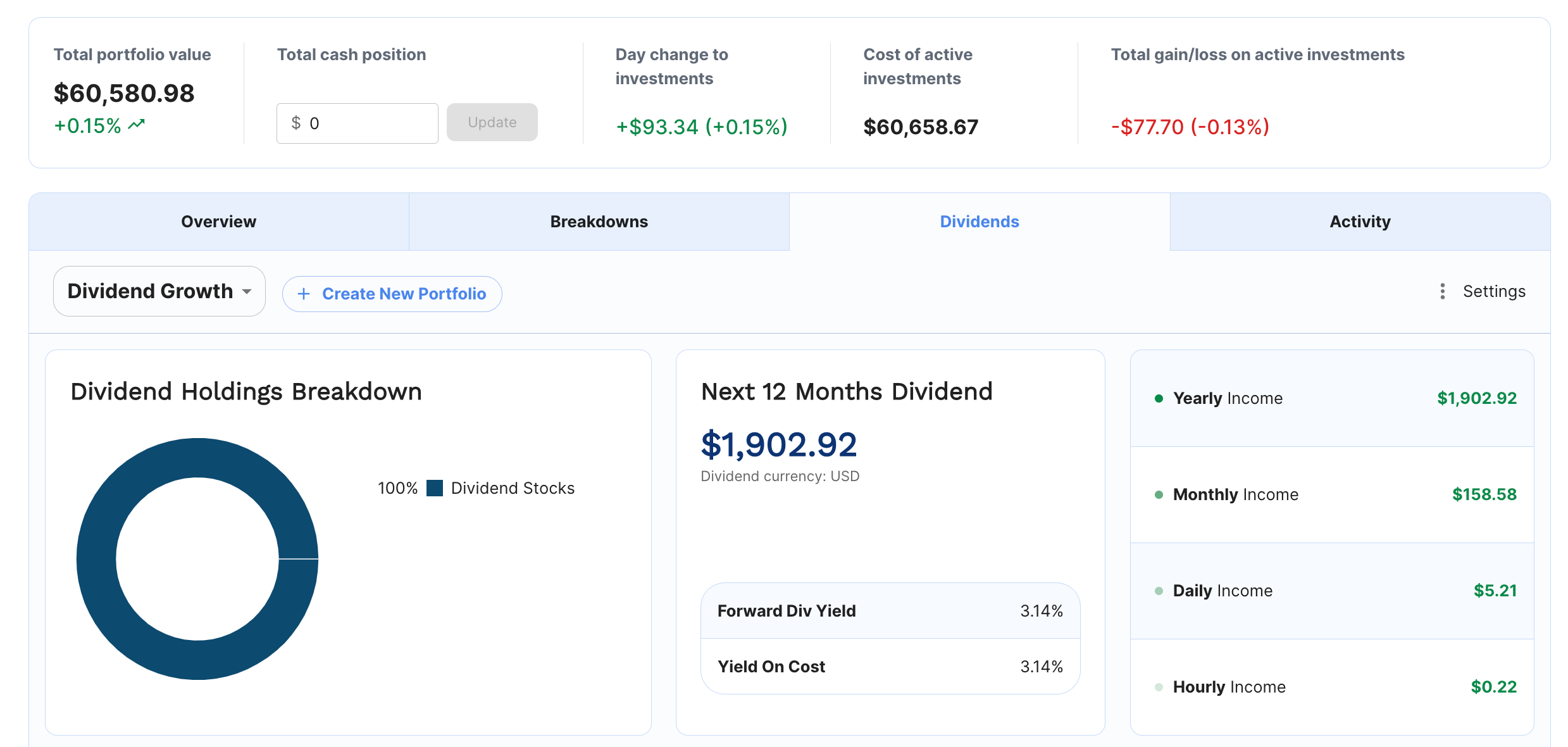

When the tracker below shows a total gain of $6,676.92 I will be in the green since inception on Feb 15, 2022.

I’m sharing that so everyone knows I’m not trying to make my performance look better than it is.

Looking at the top left corner of the image above, you’ll see 55% of the portfolio is non-dividend-paying companies. The goal of this portfolio is to beat the market on a total return basis over 5+ years without taking on excessive risk by only investing in “growth” companies. I’m also not optimizing for the highest dividend yield possible because I want a balance of dividend growth and yield.

The image below shows we have $60,580 of the $135,060 portfolio invested in dividend payers. If we look at just the dividend side of the portfolio, the dividend yield is 3.14%.

So if the entire $135,060 portfolio were invested in these dividend payers, the yearly income would be $4,240, which is $353 per month.

If you want to track your portfolio in Stock Unlock or use their DCF analysis tool and other research tools, here’s my referral link if you want to check it out.

The only change this week was purchasing more BN 0.00%↑ with new portfolio contributions. I explained why in an article earlier this week:

Lowe’s Q1 2023 Earnings

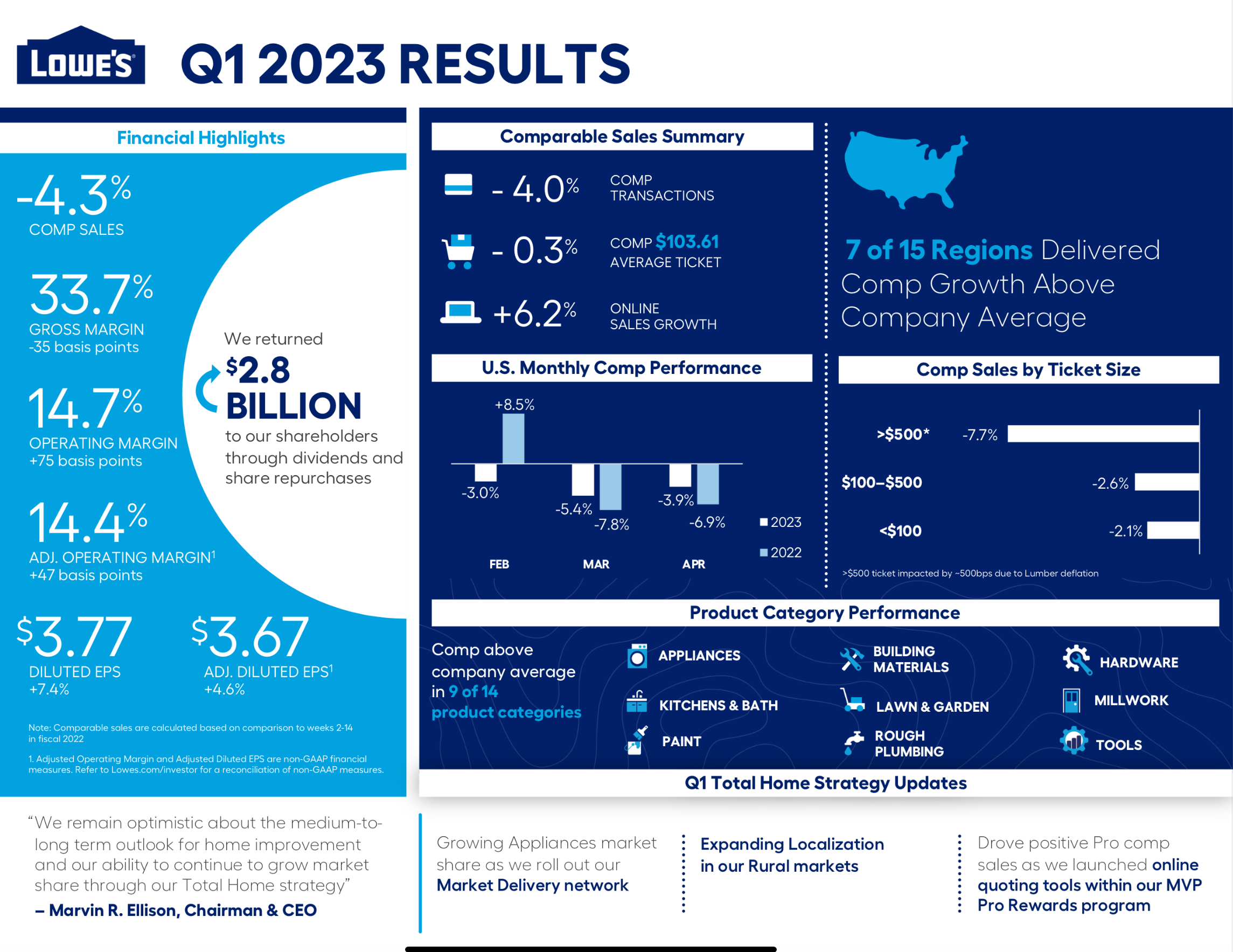

Lowe’s ( LOW 0.00%↑ ) turned in another solid quarter. Lowe’s reported $3.67 in earnings per share on $22.3B in sales. Analyst expectations were $3.45 in earnings per share on $21.68B in revenue. So for the current quarter, the business performed better than analysts were expecting. Comparable sales decreased 4.3%, which was worse than the 3.28% drop expected. Management cited “lumber deflation, unfavorable weather and lower DIY discretionary sales” for the drop.

When the results were released, the stock initially traded lower because the market seemed to be focused on management revising full-year 2023 guidance lower after beating expectations for the first quarter.

That’s a sign that management is less confident in the data they’re seeing going into the rest of the year.

For the full-year, the company lowered total sales forecasts to a range of $87B to $89B from a prior $88B to $90B. Earnings per share guidance was updated to $13.20 to $13.60, down from management’s previous guidance of $13.60 to $14.00. Finally, comparable sales are expected to be down 2% to 4%, revised downward from a previous guide of flat to down 2%.

This is not a significant downward revision and it’s important not to focus too much on any single quarter. However, anytime management lowers their own guidance, it’s an indication that something in the business environment has weakened so we shouldn’t totally ignore it.

It’s also important to remember our thesis for investing in companies. I’m invested in Lowe’s because of their established position as a leader in the home improvement industry, and management’s focus on maintaining high single digit earnings growth while returning capital to shareholders through dividends and share buy backs.

In this quarter alone, management returned $2.8B to shareholders which was over 10% over revenue. They also just increased the annual dividend by 4.8% which marks 63 years of consecutive increases.

A $10,000 investment in Lowe’s in 2003 has earned $16,445 in dividends and grown to $172,366 with dividends reinvested. Strongly outperforming the S&P 500.

Our long-term thesis is fully intact and shares are trading at a very reasonable forward P/E of 15. Now is a great time to consider adding to or starting a position in Lowe’s.

American Tower Corp at JPMorgan Global Technology, Media and Communications Conference

My biggest takeaway from the CFO’s talk at the conference is that things are just powering along as usual for AMT 0.00%↑. U.S. billings growth is on track at roughly 5% organic growth, Europe is running around 7% growth, and Africa is seeing “strong growth”. I expect AMT’s business to continue performing well driven by increased demand for mobile data across the globe.

Smith was also asked about AMT’s acquisition of CoreSite, a U.S. data center business. Here’s his view on how things have gone after the acquisition and his thoughts on some potential benefits to their tower sites from some of the data center customers.

American Tower has paid and grown its dividend for 10 consecutive years. So not as long as Lowe’s, but the total return since 2003 has been incredible. A $10,000 investment in 2003 has paid $106,512 in dividends and grown to $612,985 with dividends reinvested. Remarkable.

It’s important to note that past performance does not guarantee future results but with dividend paying companies, we can monitor their payout ratios, debt levels, and growth and have a pretty reliable perspective on their ability to continue paying and growing dividends.

Both of these companies have plenty of room to continue their dividend streaks.

Additional Reading

My friend Ian Cassel shared a link on Twitter to this Interview with Tony Deden. Tony is a wealth manager living in the Swiss Alps. What stands out to me is how intentional Tony is about totally isolating himself from the “norms” of asset management and all the noise of the daily news cycle. I also really appreciate his respect for managing peoples “permanent capital” and his focus on durable businesses.

It’s a stark contrast to how active I’ve been lately and a much needed reminder for me to focus on the very long-term.

See you Tuesday for the Perimeter Solutions deep dive.