What is Founder Stock Investing?

Our self-managed portfolio is up 201% since 2014. Investing has changed our lives

Hey friends,

Thank you so much for taking the time to read this and signing up for my newsletter.

I’m starting this newsletter because investing has drastically improved my family’s financial future. It has given us the ability to make career changes as our family situation changed and I wanted to spend more time around my wife and kids. It has given us the confidence to move back to our home state of Florida where we can be closer to our parents and siblings. We spent seven incredible years living in various places while I was on Active Duty in the Air Force which meant a lot of time missed with our families. More importantly, because of how far away we have lived, our parents have not had the opportunity to spend as much time with our kids as we would like. Sarah (my wife) and I had such strong relationships with our grandparents growing up and we want the same for our kids.

We would not have had the confidence or financial means necessary to make these important life decisions if we did not invest.

I want to share our journey with others, transparently share our investments and results, and empower others to start investing.

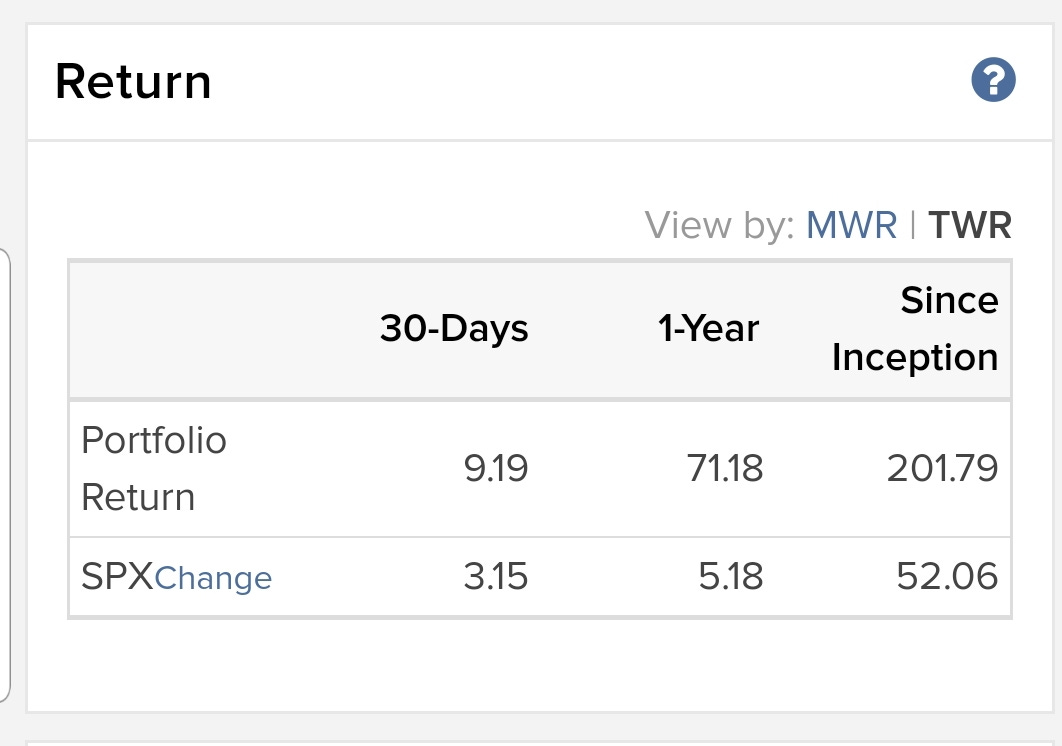

Background and results since November 2014

I’m not a professional investor, I don’t have a business or finance degree, and I’ve worked a full-time job (sometimes with no access to the internet) the entire time I’ve been investing.

I say all of this because there’s a myth that professional investors have some secret sauce and that us mere mortals aren’t intelligent or capable enough to manage our own money. That couldn’t be further from the truth, we’ll get into how individual investors like you and me can grow incredible long-term wealth and beat these “professionals” in a future post.

Since November 2014, our portfolio has increased by 201.79%. As a comparison, the “market” which just means the S&P 500 index has returned 52% during that time. The S&p 500 is basically 500 of the largest companies in America that are believed to give a good indication of how the stock market is performing. This is as far back as I can measure performance because that’s when I switched to the current brokerage I use which is where I pull all performance reports from.

The takeaway here is that these results prove it is possible for us to beat the market and most professional investors. One quick note, we still invest in things like our work sponsored 401k retirement plans or military TSPs. We contribute up to the match for those accounts and put them into something like a Vanguard or Fidelity S&P 500 fund for our 401ks, or the C-Fund for the TSP. When I reference our portfolio, or share performance numbers, I’m sharing information about our Roth IRAs and a non-retirement brokerage account. These are the accounts we use to invest in individual stocks.

How we Invest

In order to be successful, there are three foundational rules I follow. I would not be successful without them.

We don’t invest any money we might need in the next three years. This helps me avoid the temptation to fall prey to all of the negative headlines in the news. Bad things will certainly happen and there will definitely be recessions in the future. But no matter what anyone tells you, it is impossible to know when. More money is lost by people waiting to start investing until the next recession than is actually lost during recessions (especially if you’re invested in great companies and don’t sell). Great companies will recover just fine after recessions and the fact that we don’t need the money we have invested for at least three years means we can stay invested and not panic.

We aim to save/invest 20%-30% of our income each month. Some people save less, some save more. The important thing is to save what works for you. Start with 5% or 10% if that’s what work and try to grow that over time as debt is paid off or your get raises. What this does for our family is gives us a mental buffer. We know if an emergency were to happen before we ever had to dip into our savings or investments, we could shift that 20%-30% towards whatever unexpected expense comes up. This really helps us sleep well at night. Beyond this, we don’t do any budgeting and spend money on whatever we want. If we’re saving 20%-30%, paying all our bills, and not taking on debt, then our budget is just fine. I’m not knocking budgeting here. I just know myself and know I could never keep a detailed budget.

When we invest in individual companies our goal is to find incredible companies with incredible management (usually founders of the company…95% of the time) and stay invested in those companies for 5+ years. The truth is it is impossible to know what will happen in the short-term. However, over the long-term, exceptional companies do very well. Think about companies like Starbucks, Disney, Apple, Google, Netflix, etc. Those companies have had their ups and downs, but over the long-term they have been incredible investments for people who stuck with them. We want to find the next generation of companies like those and stick with them. You simply can’t do that with day-trading or penny-stocks (see below).

What we don’t do

I’ve seen a lot of scam artists out there trying to trick people into day trading, penny stocks, worthless but expensive courses, and whatever else. I don’t do any of this with one caveat. There are a few occasions where I have made short-term trades (basically a gamble) with 1% of our portfolio. This is a terrible habit, it usually results in losing money, and it’s literally not worth the time or stress so I’m doing my best to stop. For whatever reason, I just get the itch to do that every once in a while and to be honest, it’s embarrassing. Fortunately it has not been detrimental to our portfolio, but that’s the type of thing that can get out of control.

What should readers expect?

Through this newsletter, I plan to share the resources I use, what I’m reading, our transactions, and portfolio updates transparently. My hope is that I’ll educate, inspire, and empower others to take control of their finances, begin investing, and take control of their financial futures.

The next few posts will be about the criteria I use to find companies to invest in, earnings report reviews from Mongo Database (MDB), StoneCo (STNE), Smart Sheets (SMAR) which are all companies we own, and at the end of March (and every month) a monthly portfolio review updating our holdings and performance for the month.

Thanks so much for reading. If you’ve made it this far and find this valuable, I’d love for you to share with a friend and also let me know how often you’d like to get emails/updates from me? Once a week, twice a week, or whenever something happens that’s worth writing about?

Best,

Austin