Weekly Review: Up $21,449 (3.5%)

Sold Roku, Added Datadog

Hey everyone, hope you’re having a wonderful week. It felt good to have a positive return on the portfolio this week after losing 16% last week and roughly 2% the week prior. This is an extremely short time frame and we’re long term investors, but watching that much money melt away is never fun. We’re still up 29% YTD which is wonderful and still outperforming the S&P500 which is up roughly 20% YTD.

More importantly than any of that, our daughter had a relatively minor surgery and is recovering well. Just a reminder to remember WHY we invest. For me investing is supposed to enable us to spend more time together as a family not consume me and make me spend less time with them (or be less present). Unfortunately, sometimes it does distract me from family, but I’m working on it.

7-Day Return:

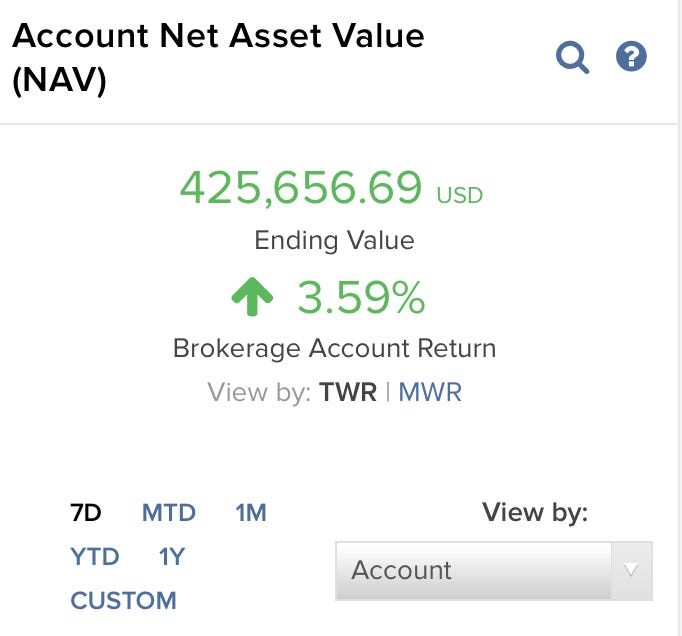

Starting Value: $403,897

Ending Value: $ 425,347

Change: +$21,449

Change %: +3.52%

Portfolio Changes

This week was a bit hectic for us. Our 2yr old daughter had some minor surgery scheduled on Wednesday, September 18. She’s recovering well, and we’re blessed that our kids have had good health. I know many families are not as fortunate and have to deal with much harder situations. However, it’s still hard when anything like that happens to your kids.

Why am I bringing this surgery up? Probably because I share way too many personal details in this little newsletter, but also because these are the real situations and stressors that people deal with. I don’t remember ever having the lesson “how to deal with your finances before, during, and after your kids have surgery” and these are the types of topics that are most important because unexpected things happen.

Anyways, we were at the hospital almost all day on Wednesday between registration, pre-op, surgery, and recovery. Wednesday happened to be the day that Comcast announced a competing product to Roku. Here’s a timeline of my feelings towards Roku and what ultimately led to me selling.

Prior to Wednesday, September 18: we had invested about 5% of our capital into Roku which was up nicely to around 7.5% of our portfolio. I was happy with the returns but feeling uneasy about the company.

I’ve never been 100% comfortable with Founder and CEO Anthony Wood. I don’t know any conspiracy theories about him, but he was the Founder of Tivo which to my knowledge ended up underdelivering on high expectations, but more importantly than that, I’ve just never felt like he is 110% behind Roku as his life’s passion. He says great things like “have a Roku device in every home” but I just don’t feel it. Here’s an example from a recent keynote.

Roku doesn’t appear to be an amazing place to work. I want to own companies that attract the best talent and from my very basic investigative skills, Roku just doesn’t check that box for me. The company has a Glassdoor.com company rating of 3.7 and a CEO approval rating of 78% versus a company like The Trade Desk which only has a marginally better company rating of 3.8% but a 94% CEO approval rating. There are other factors like the impression I get by viewing a company’s website, workplace type awards, etc and this certainly doesn’t paint the whole picture, but it’s a factor in how I invest.

I want to own the best companies in the world.

I was struggling with how much larger Roku can grow (compared to other companies I could invest in). It was sporting around a $17B market cap and Roku players/TV were already installed in something like 1/3 of TVs in the U.S. The company claims they could be installed in every TV, but I struggle to imagine that happening.

Roku is a software company but they rely heavily on hardware companies (TV makers) to get their players into people’s homes. That just feels like a lot of tough relationships to manage especially as we start to talk about international growth. I feel like there has been a 90%+ turnover in TV makers even during my short (and incredibly handsome) lifetime of 30ish years (+- 10).

So I was feeling all of those things but did nothing because generally I let numbers speak for themselves and Roku’s quarterly numbers have been great. This is what makes investing so challenging (and interesting) the battle between quantitative numbers and qualitative factors/investor feelings.

September 18: news about competition comes out and I didn’t think about it much because we were focused on our daughter. Here’s an article from Daniel Sparks, one of my favorite Motley Fool writer summarizing the news and the immediate reaction: Are Roku Investors Overreacting to Comast’s Free Streaming TV Box?

September 19: I began a very official and thorough poll of the entire world aka my Twitter network. Asking people to vote on Roku or Datadog (DDOG) as which is the better opportunity. I didn’t really weigh the outcome of the poll in my decision-making process because everyone’s situation is different. But I did have some great discussions via Twitter with people who I respect and who are/were bulls on Roku. The link below will take you to all of those tweets. I love Twitter threads like that because there are so many interesting viewpoints from so many different backgrounds (casual consumers/investors (like me), Motley Fool writers, day traders, etc).

Once I start seriously doubting a company I’m invested in or think there’s a better place for my money, I’m usually pretty quick to sell which is exactly what I ended up doing with Roku. Datadog was IPOing and I knew I wanted to open a small position so my mind was made up. A good thread on that below:

September 20: Roku ended up closing higher on the 19th than where I sold it at but that doesn’t make the sell decision right or wrong. That would be “resulting” which Annie Duke talks about in her great book “Thinking in Bets” (affiliate link).

The stock ended up dropping $25.71 a share on the 20th and closing at $108.05. Selling at $129.10 saved me $4,020. BUT this doesn’t mean it was a good decision to sell either. The whole point is that in the short-term, process matters far more than the result because no one knows what’s going to happen in the short term. I don’t know if Roku will be a good or bad investment moving forward. All I know is that I believe there are better companies for me to invest in based on my assessment (I could be totally wrong).

Why I bought Datadog

I like to invest in what I believe are the best Founder-led companies around. Datadog’s numbers are up there with Zoom and Crowdstrike’s when they IPO’d. That’s rare company and I believe all three are fantastic companies. They are selling at Price to Sales ratios (definition) of 50, 36, and 34 respectively and growing revenue YoY at 96%, 94%, and 79%.

Very high P/S ratios and very high revenue growth. With these types of companies, my approach is to start a ~1% position, then look to add over time as the IPO excitement dies down or if the company sells-off for no business-related reason.

Datadog (DDOG) S-1 Review by Alex Clayton. I recommend reading the entire S-1, but here’s an excerpt of company metrics that are impossible not to like.

Datadog ended last quarter with 8,846 total customers, 594 of which are paying more than $100K+ in ARR and 42 that are paying $1M+ in ARR. The top 10 customers represent ~14% of total ARR and no single customer represented more than 5% of ARR.

Last quarter the average customer was at $37,631 in implied ACV (implied ARR / total customers). Most of their ARR, 72% last quarter, comes from those 594 customers paying $100K+.

For the first 6 months of 2019, over 35% of new ARR came from Datadog’s newer platform products, APM and logs, up from over 10% in the same period a year earlier.

Datadog’s dollar-based net retention rate was 146% in the first 6 months of 2019 and 2018 and 151% in CY’18. Their dollar-based gross retention rate has been in the low-to-mid 90% range.

~24% of their ARR came from customers outside of North America in 2018.

~35% of the Fortune 100 were Datadog customers, while only about 20% were customers with ARR of $100K+.

Subscription agreements are primarily monthly or annual, with some quarterly, semi-annual and multi-year. Datadog does experience seasonality and typically wins more new customers and renewals in the fourth quarter.

In the first 6 months of 2019, ~60% of Datadog’s increase in revenue was attributable to growth from existing customers.

Datadog’s customers have many end-users of their products — they call out a couple of examples: a leading communications software technology provider has almost 800 Datadog users, about half of the company’s total employee count and greater than the total number of the company’s engineers. Another company, a Fortune 500 financial services firm, has over 3,000 Datadog users.

In 2019 Datadog signed an agreement with AWS where they are required to purchase at least $225M of cloud services from AWS through April of 2022.

What else did I do?

Long-time readers are going to be so disappointed in me… but give me a chance (it’s different this time) OPTIONS!!!!!!

Okay, options are not required for investing success and in fact, they are a great way to destroy returns. Options trading has actually destroyed somewhere between 8%-10% of my return this year which is just reckless. However, that was silly/stupid day-traderish (sorry day traders, I’m talking about myself here) options trading.

There are longer-term options on companies I already own and would be happy to buy more shares of at a lower price. So that’s how I used options this time. Please don’t get involved with options unless you 100% know what you are doing with them.

I sold puts on companies I already own which gives me the obligation to potentially buy 100 shares per contract if the stock is below a certain price before or on a certain date. Here’s how those work in action.

Crowdstrike: we own 110 common shares with an average purchase price of $75.78. Those shares represent 1.73% of our portfolio. I would be more than happy to buy 100 more shares at a lower price so..

I sold 1 x January 17, 2020 $60 strike put for $5.40. Remember 1 contract represents 100 shares

That means I was paid $540.00 and now have the obligation to buy 100 shares of Crowdstrike at $60.00 per share if the company trades below $60.00 between now and January 17, 2020. If we subtract the premium we were paid from the strike price, we find out what price (or below) this trade becomes unprofitable.

So $60 - $5.40 means this will be profitable if Crowdstrike is at or above $54.60 between now and January 17, 2020. If Crowdstrike stays above $60, we keep that $540 and our option contract expires on January 17th relieving us of that obligation to buy shares.

Pagerduty: we already have a roughly 5% position in Pagerduty and I sold 2 x $25 strike $Feb 21, 2020 Puts which means we are obligated to purchase 200 more shares at $25.00 if the stock trades below $25 between now and February. That would increase our position by about 1%. We were paid a premium of $3.49 ($349) per contract which means our break-even price is above $21.51 per share.

Zoom: same deal with Zoom. We have a roughly 4% position in Zoom which I’d be happy to increase by about 1% if the stock trades lower.

Sold 1 x $65 strike Jan 17, 2020 Put and received a premium of $4.24 ($424) which means our break-even price is above $60.76 per share.

Zscaler: sold 2 x $45 strike Jan 17, 2020 Puts for a premium of $3.65 ($365) per contract which means our break-even price is above $41.35 per share.

We received $2,392 in premiums and are obligated to purchase $26,500 in shares of companies we love at prices 15%-25% lower than they are selling at today. If the shares are all above their strike prices by expiration, we keep that $2,392.

The key here is that we have to be willing and able to purchase all of the shares we are obligated to purchase if these don’t work out. These are companies I want to own long term and would be happy to buy more shares at those lower prices.

Thank You

Thank you all so much for reading and helping to support my goal of making investing accessible to anyone with an internet connection. We are now at 944 total subscribers and 63 paid subscribers which brings in roughly $3,000 (before taxes). If you enjoy this please hit the ❤️ at the top of the page (this helps others find us on substack.com), share with friends, and/or start a paid subscription for $5/month or $50/year.