Weekly Portfolio Update. -11% Down $40,000

Everything is totally fine!!!! Seriously......I think?

This update was written mostly on Friday, October 18th and Saturday, October 19th but I got busy with life and didn’t post it. So pretend you’re reading this over the weekend. All portfolio performance numbers were as of Friday, October 18th.

Last week I called the end of the #SaaSpocalypse. Oops.

Clearly, I made the investing spirits angry (sorry everyone) because this week was painful.

We were down 11% this week which brought the portfolio down roughly $44,000. That’s a ton of money (to our family) and it certainly hurts to look at so please don’t take my sarcasm the wrong way. I do like to have fun and I do believe that in 5-10 years, this will look like a great buying opportunity in these companies. We just have to make sure we set ourselves up to stay invested that long.

The last 7 days have been horrendous. But whether times are good or bad, I think it’s important to stay focused on the long-term.

Over the last 12 months, we’re up 13% and beating the S&P500 by 1.5%.

Since inception (November 2014), we’re up 158% and beating the S&P500 by 96%.

I’m always learning and tweaking, but I’m fully confident in my process and I’ll continue to stay fully invested in what I believe are the world’s best Founder-led companies.

What I did this week

Monday, October 14: 0 transactions

Tuesday, October 15: 0 transactions

Wednesday, October 16: 4 transactions

Sold 20 shares of MDB for $133 per share (tax-loss harvesting. I still have a ~15% position in MDB. Will likely add after 31 days)

Sold 429 shares of WORK for $23.75 (tax-loss harvesting + wanted to invest in ROKU. I still own a little WORK in our rollover IRAs and I’ll probably leave those shares alone because I’m lazy. I do believe in this company long term.)

Sold 50 shares of PLAN for $47.28 (tax-loss harvesting. Still have a ~6% position in PLAN.

Bought 125 shares of ROKU @ $134.19

Thursday, October 17: 7 transactions

This is where things got weird and I decided to open up some earnings-related straddles (buying a put and call at the same strike price for the same expiration date) on a few companies with about ~5% of my portfolio. I’m not proud of the fact that I did this. It goes against my fundamental beliefs of being a long-term investor and I know it will likely end up in my losing money and being mad at myself but…. I did it.

Why? Well, I think that either these companies will be volatile (either up or down) after earnings, or the market, in general, will be volatile which could make these companies move a lot up or down.

So here we go. I’ll arrange these by earnings date:

Earnings date: Thursday, Oct 17

Bought TEAM: Nov 01, $123 straddle for $12.69. So basically, I needed the stock to move to $110 or $136 to be profitable.

Bought ISRG: Nov 01, $532.5 straddle for $28.5. Needed about a move to $504 or $561 to be profitable

Earnings date: Tuesday, Oct 22

Bought SNAP Nov 01, $13.5 straddle for $2.16. Need a move to $11.25 or $15.75 to be profitable

Earnings date: Wednesday, Oct 23

Bought ALGN Nov 01, $215 straddle for $22.20. Need a move to $191.78 or $238.22 to be profitable

Bought NOW Nov 01, $255 straddle for $25.27 need a move to $228.38 or $281.62 to be profitable

Bought TSLA Nov 01, $262.5 straddle for $25.8 need a move to $237.23 or $287.77

Earnings date: Monday, Nov 04

Bought NBIX Nov 15, $95 straddle for $9.35 need a move to $85.09 or 104.91

Friday, October 18: 8 transactions

Sold TEAM $123 Puts for $9.90. This means our TEAM straddle is no longer a straddle. The stock was down between 4% and 8% throughout the day. So two things can happen from here.

Scenario 1: the stock will stay below $123 and my calls will expire worthless. In this scenario, I’ll lose the difference between the $12.69 premium I initially paid for the straddle and what I sold the Puts for. So worst case, I lose $2.79 per contract. I had 5 contracts and each contract represents 100 shares so total loss here could be $1,395.

Scenario 2: the stock recovers between now and November 01 to above $126 which would make this a profitable straddle. This is possible but unlikely.

Sold ISRG $532.5 Calls for $36. This means our ISRG straddle is no longer a straddle. The stock was up between 5% - 8% throughout the day so I sold our calls. Our two possible scenarios are

Scenario 1: the stock stays above $532.5 and the puts expire worthless. In this scenario, our profit will be the difference between the $28.5 premium I paid and what I sold the calls for. Worst case scenario, our profit on this straddle will be $36 - $28.5 = $7.5 per contract. We had 2 contracts which represent 100 shares each so thats a profit of $1,500.

Scenario 2: the stock falls below $532.5 and I can sell the puts to collect some additional premium.

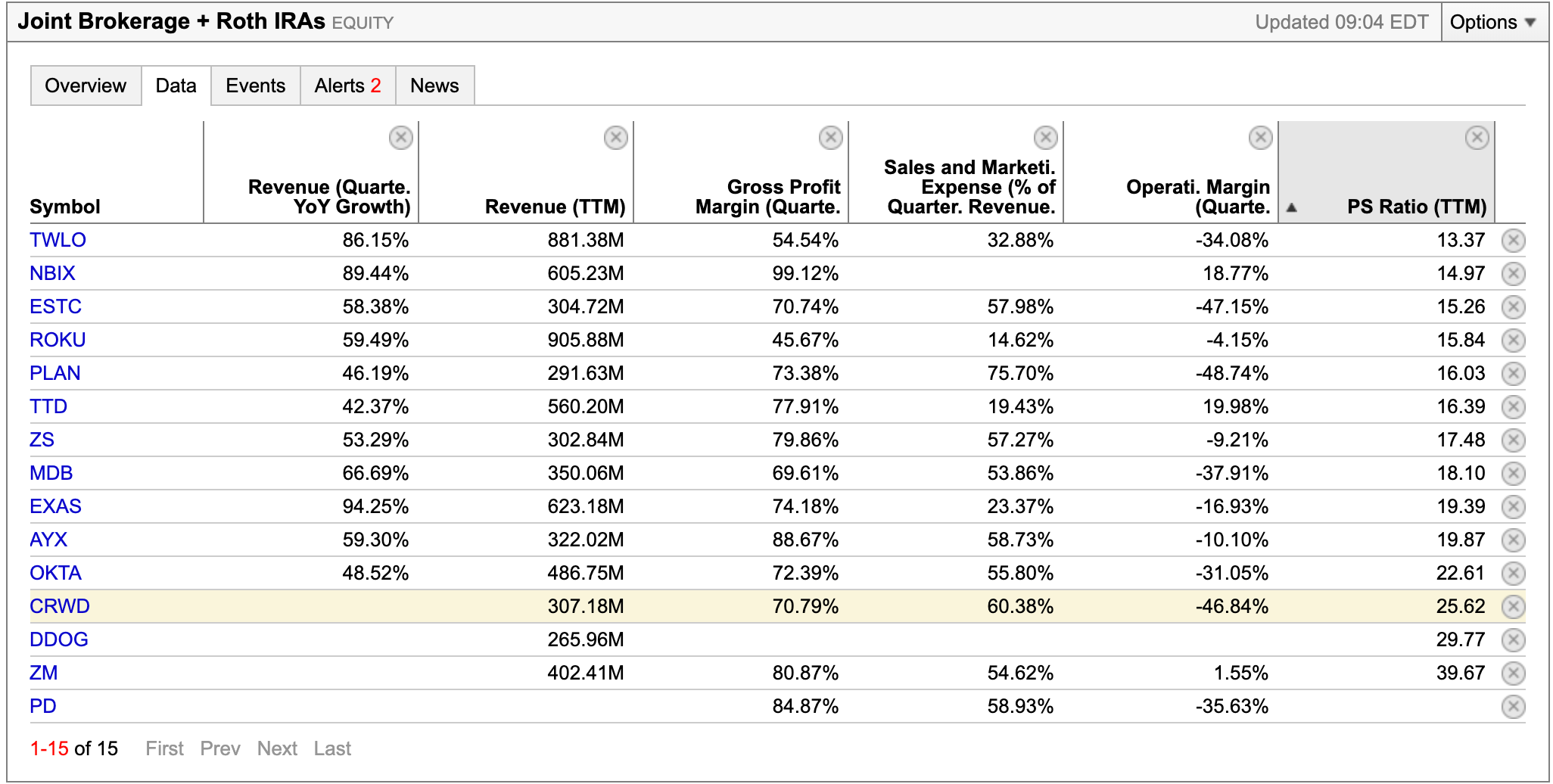

Sold 101 shares of OKTA from our non-taxable accounts. Okta is a $11.8B market cap company with a PS ratio of 22.61, is growing revenue at 48.52% YoY with a Gross Profit Margin of 72.39%. I still have a roughly 5% position in OKTA, but I wanted to add shares to companies I feel are better current opportunities.

Bought 10 shares of NBIX for $95.20. I’ll probably leave this position alone and just see what happens. At most, I could see myself doubling it over time, but since pharmaceutical companies can be extremely volatile and risky, I don’t see myself ever allowing this position to become larger than 2% of the portfolio.

Bought 20 shares of EXAS for $96.90. Same deal as NBIX. I’ll probably just leave this one alone and see what happens.

Bought 40 shares of DDOG for $33.32. I believe Datadog is one of the best companies around and I plan to continue building up this position. It’s currently a 2.5% position and over time I’d be comfortable with this as a 10%+ position. Datadog has a $9.26B market cap with a PS ratio of 29.77, YoY revenue growth of 96% (FY 2018 vs FY 2017) and gross margins of 74%. So Datadog has a rough 10% smaller market cap and a 30% higher PS ratio than OKTA. But DDOG is growing revenue roughly 100% faster with higher gross margins.

Bought 30 shares of ROKU for $130.47. If you’ve read my newsletters for any period of time, you know my on-again-off-again relationship with ROKU. I need to just own the darn shares and leave them alone. I keep getting in my own way here because I personally am not a user or fan of Roku devices. However, the numbers are outstanding and Apple’s latest move to partner with ROKU shows the value of Roku’s neutral stance in the streaming TV space. Roku is a 5% position in my portfolio.

Bought 30 shares of ESTC for $71.15. Elastic is an extremely complicated company that does mostly internal search type magic for companies. They recently jumped into the endpoint security market by acquiring Endgame which makes them competitors to CRWD. I like all of the growth drivers behind Elastic and I’ll likely trim some shares of CRWD in the coming weeks for tax-loss harvesting purposes so Elastic feels like a good replacement. I’m not sure about selling CRWD shares yet because their growth is so impressive….need to think about it more.

Here’s a look at some of the important data points I look at. This shart is ordered from the lowest PS to the highest PS. TWLO’s YoY revenue growth is not really 86%. That was boosted by the Sendgrid Acquisition. Also, PD, DDOG, CRWD, and ZM aren’t showing YoY revenue growth because of how recently they IPO’d. But they are growing revenue YoY at 45%, 97%, 94%, and 96% YoY But this helps explain the shift away from OKTA and into more ROKU, ESTC, and DDOG.

Current portfolio and position sizes

Some changes to the newsletter

Last week, I asked for our community’s thoughts on whether I should continue with weekly portfolio performance updates or move to them to monthly. I received some incredible messages and many of you encouraged me to move to monthly. My sanity thanks you.

I’m excited about this because it will allow me to continue being fully transparent while giving me time to share deeper dives into the companies I’m invested in and new companies I’m considering buying shares of. So I’ll still be emailing & podcasting weekly, but I’ll only do performance updates once a month.

As always, thanks so much for reading. If you want to support this newsletter, hit the ❤️ at the top which helps with discovery, subscribe to the “Founder Stock Investing” podcast, share on social media, and/or start a paid subscription for $5/month or $50/yr.

I’ll be back with updates to my stupid options trades.

- Austin

Hi Austin, your weekly updates often mention the *market capitalisation* of the companies you invest in. Does the size of their market cap imply something about the strength of their business? For instance; what did Nortel Network's market capitalisation in 1999 say about the quality of their business?