ServiceNow Deep Dive

Why I'm buying after this 50% drop

ServiceNow is one of the companies that I keep coming back to. I’ve always thought it was a great company, but in recent years, I felt the stock was just too overvalued. After a 50%+ drawdown due mostly to AI fears, I think the stock is now too undervalued to ignore and presents a great opportunity for long-term investors.

So I’ll be adding it to The Growth Curve Portfolio and I thought it was a good time to do a deep dive on the stock.

I’m making this deep dive 100% free. If you find it valuable, please share it and consider starting a paid membership for more deep dives and to get all of my portfolio/trade updates.

The Big Picture

ServiceNow started as an IT help desk ticketing platform. Then, over the past decade, it quietly became the operating system for large enterprises, and today it sits at maybe the most interesting intersection in enterprise software: the point where AI stops being a chatbot and actually gets work done.

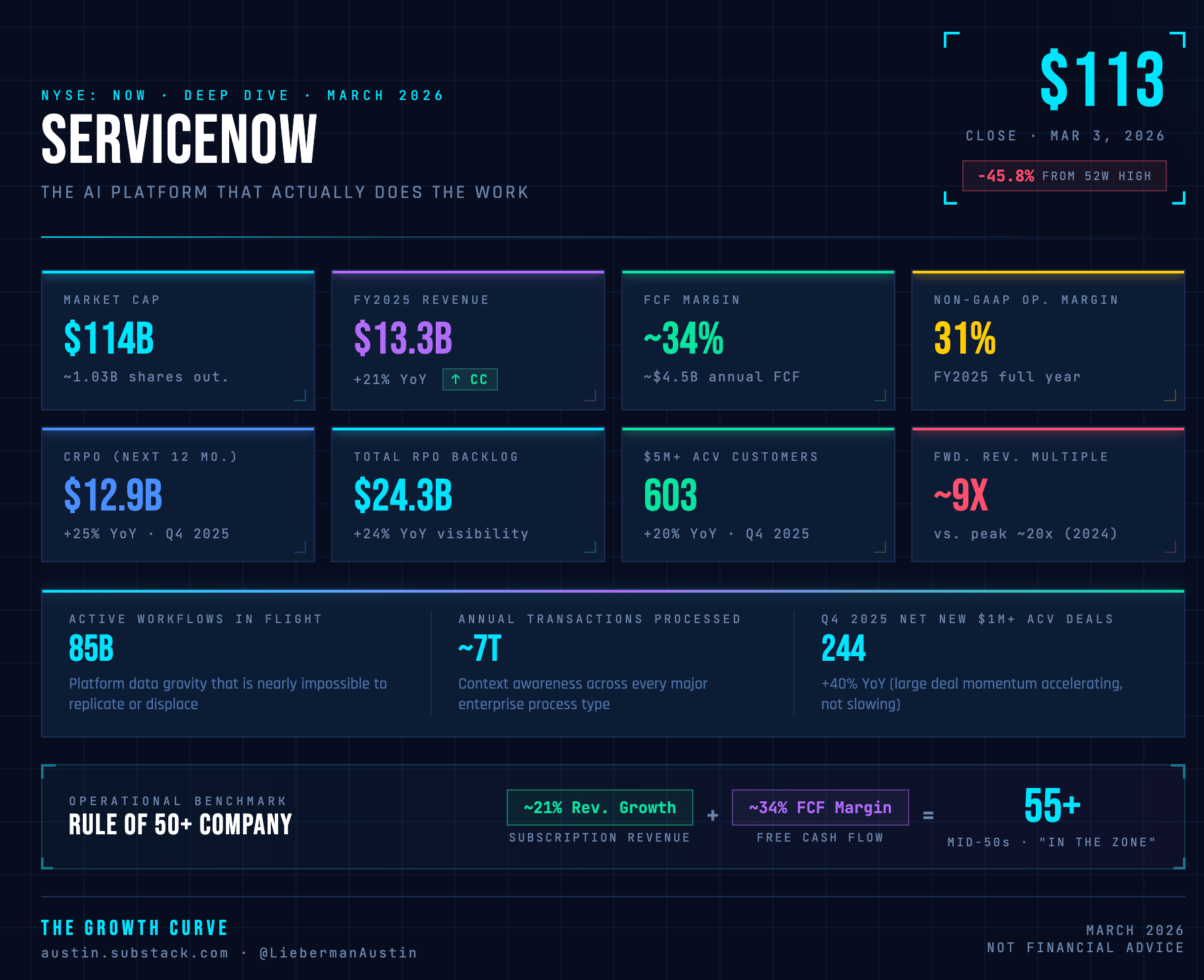

The stock has been absolutely crushed since mid-2025, down roughly 53% from its all-time high near $239. At $113 and a $114B market cap, you now have a company growing revenues north of 20% annually, generating ~34% free cash flow margins, and sitting on $12.85B in current remaining performance obligations, trading at less than 9x forward revenue. That is a different conversation than it was 12 months ago.

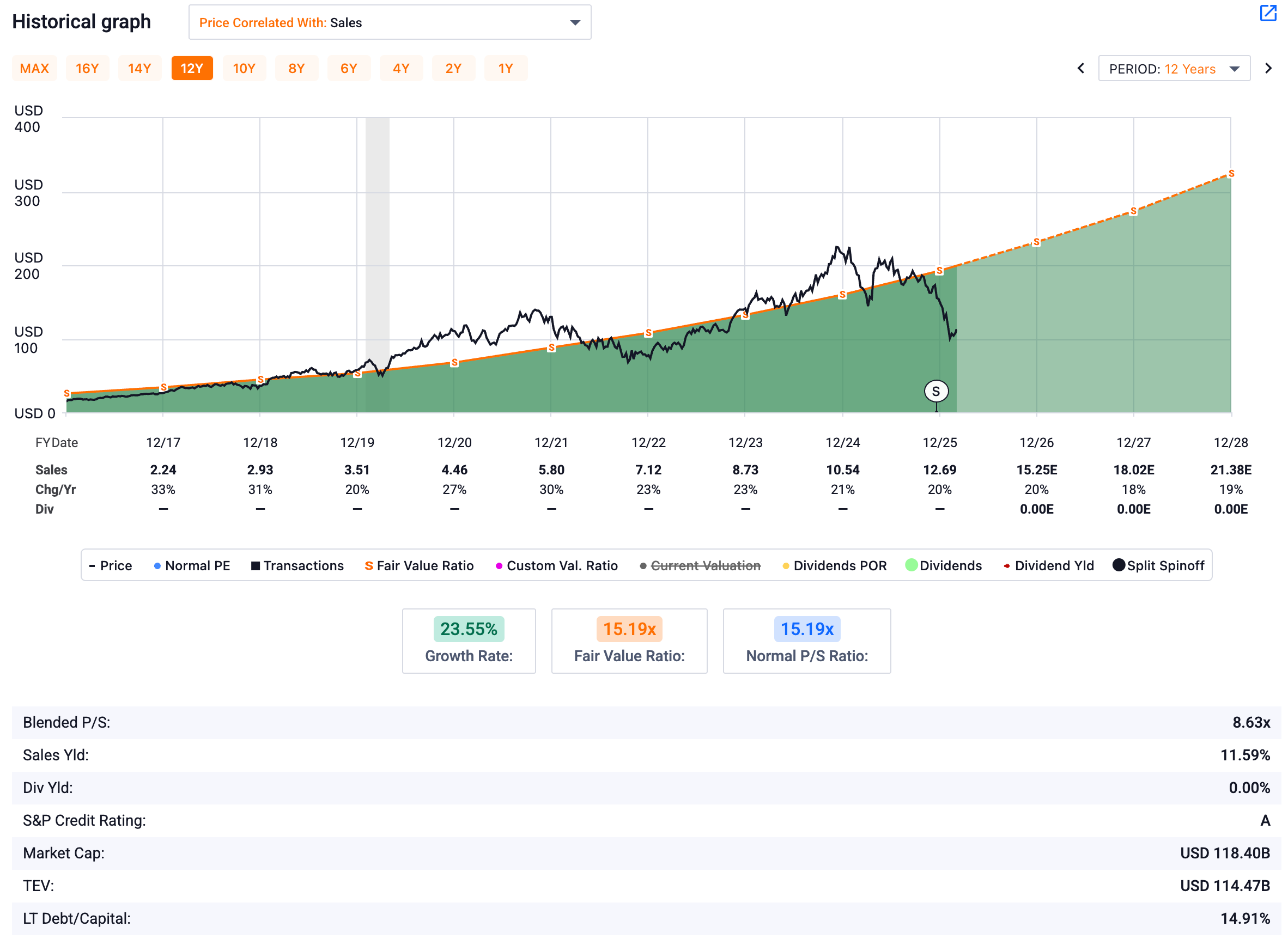

The FAST Graphs chart below immediately shows how severe the drawdown has been and how undervalued the stock is compared to its average P/S multiple over the last 10 years.

Right now, the Blended P/S is 8.63 while the 10-year average is 15x. Everyone knows the stock has sold off and it’s clearly trading at a discount to its historical average but the question that really matters is whether or not the AI disruption fears for NOW are real.

That’s the focus of this deep dive.

If you’re a FAST Graphs subscriber, here’s a link to the NOW Chart.

If you’re not a FAST Graphs subscriber, this link will give you a 7-Day free trial and 25% off a subscription if you decide to try it out.

What Does ServiceNow Actually Do?

The simplest way I can put this: ServiceNow is the control center for enterprise workflows. Think about what happens inside a big company when something breaks or someone needs something done. An employee submits a ticket. That ticket has to route through approvals, trigger tasks across multiple departments, update records in legacy systems, and eventually get resolved. For most companies, that process involves switching between 10 - 20 different tools. ServiceNow replaces all of that with a single platform.

It started in IT service management (ITSM), which is still the core and is still growing well. But from there, the company expanded into HR service delivery, customer service management, security operations, financial workflows, and recently, agentic AI. The platform now handles roughly 85 billion workflows and nearly 7 trillion transactions across the global economy. ServiceNow is entrenched in the operating layer of key enterprise processes. It’s not just some application that employees use, which makes it very sticky and hard to disrupt.

Here is the key insight that Bill McDermott keeps hammering: a large language model can tell you how to fix your VPN. ServiceNow can actually fix your VPN. That distinction, between thinking and doing, is the entire thesis.

Business Model

Revenue is predominantly subscription-based, representing over 97% of total revenues. Customers sign multi-year contracts, typically 3 years, with near-automatic renewal given how deeply embedded the platform becomes. The company prices based on active users (seats), though it is actively building out a hybrid consumption-based model for its AI products. Management refers to this as the “Pro Plus” tier, where customers get a bundled allotment of AI capabilities and then reload tokens as usage scales.

The financials are exceptional. FY2025 total revenue came in at $13.3B, up 21% year-over-year. Non-GAAP operating margins run around 31%, and free cash flow margins hit approximately 34%, meaning the company generates roughly $4.5B in annual free cash flow. It also operates what McDermott calls a “Rule of 50” company, meaning the combination of revenue growth rate plus free cash flow margin consistently exceeds 50 (currently in the mid-50s).

Customer metrics are healthy and accelerating. At year-end 2025 there were 603 customers generating over $5 million in annual contract value, up roughly 20% year-over-year. Net-new deals with ACV over $1 million in Q4 2025 hit 244, up nearly 40% year-over-year. The cRPO of $12.85 billion growing 25% gives excellent visibility into the next 12 months of revenue.

The AI Strategy: Action, Not Just Answers

The core AI product is Now Assist, ServiceNow’s suite of generative AI capabilities embedded directly into workflows. Unlike standalone AI tools, Now Assist sits inside the workflow context, so it can not only answer questions but trigger actions, pull records from connected systems, and resolve issues across the enterprise automatically. Management guided to $1 billion in Now Assist ACV by 2026.

The broader AI vision is something McDermott calls the AI Control Tower. This is where NOW’s recent acquisitions come in: Moveworks (employee experience, AI front door), Veza (identity and access management for humans, machines, and agents), and Armis (OT/IoT asset security). Together these acquisitions allow ServiceNow to manage not just human workers but also the growing fleet of AI agents being deployed inside enterprises. Think of it as ServiceNow becoming the HR department for both people and bots, onboarding them, monitoring them, governing them, and securing them.

The Armis acquisition in particular looks interesting to me. Armis already works with 40% of the Fortune 100, has essentially no dedicated sales force, and covers operating technology (OT) security, meaning physical infrastructure, IoT devices, manufacturing equipment. Combined with ServiceNow’s existing IT platform and distribution, the potential CAGR expansion here is significant.

Competitive Position

The most common competitive worry you will hear is that Salesforce, Microsoft, or some LLM startup is going to eat ServiceNow’s lunch. Let me be direct about this: I believe that concern is overblown (leading to this sell off), though it is something to watch.

ServiceNow’s moat comes from workflow data gravity. Once an enterprise runs thousands of workflows on ServiceNow, pulls data from its ERP, HR system, security tools, and CRM into the platform, and trains employees to work within it, the switching cost is enormous. The average employee reportedly uses an average of 20+ applications per day at large enterprises. ServiceNow collapses that into one platform. That is not easy to displace.

On the Salesforce question specifically: McDermott directly addressed the ongoing competitive noise at the JMP Technology Conference, noting ServiceNow currently has $2 billion in CRM pipeline, and highlighted Nvidia, DraftKings, Starbucks, and Micron as customers choosing ServiceNow’s CPQ and CRM capabilities. Nvidia’s team apparently called ServiceNow CPQ the best in the industry for configuring AI data center installations.

The real competitive risk is not displacement. It is consumption-based pricing disruption if AI agents dramatically reduce the number of human seats enterprises need. Management is actively building the hybrid model to address this, but it remains the most legitimate structural question investors should monitor.

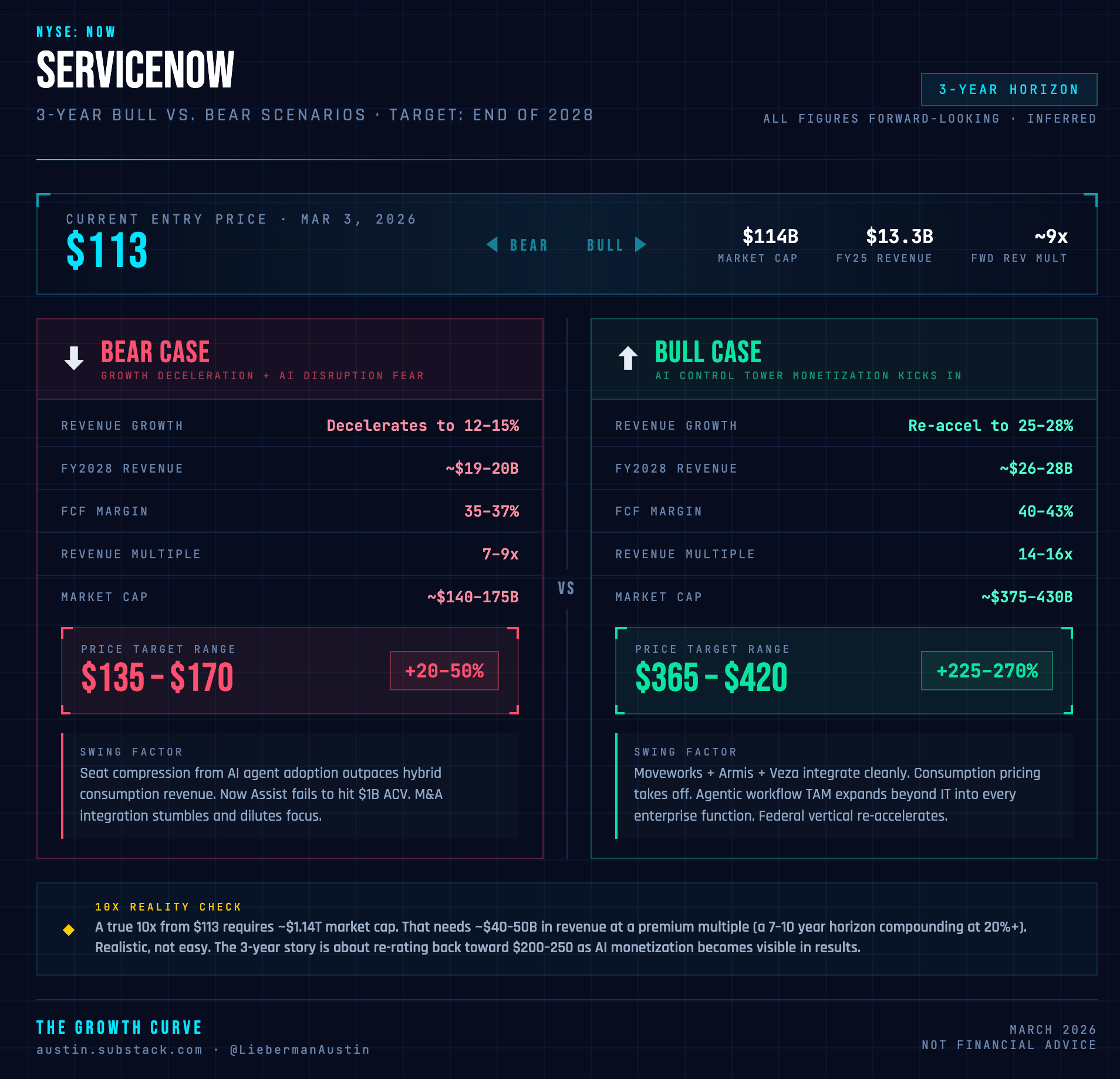

What Would Have to Happen for a 10x Return?

At $113 per share and ~$114B market cap, a 10x return means reaching roughly $1.14 trillion in market cap within a reasonable timeframe. That won’t happen in three years but let’s think about what the math looks like over a 7-10 year horizon.

A $1T+ market cap at a 20-25x revenue multiple implies roughly $40-50B in annual revenues. If ServiceNow grows at 20% annually from $13.3B in 2025, it reaches approximately $40B by 2033 and $48B by 2035. That is an aggressive but not unrealistic trajectory, particularly if AI monetization adds a meaningful layer above the base subscription business. The company’s $10B revenue target by end of 2026 is already well within reach given cRPO visibility. A $40B revenue pathway would likely require successful monetization of the Armis OT security opportunity plus significant AI consumption revenue on top of the seat-based model.

From today’s price, a more realistic 3-year question is whether the stock can get back toward $200-250 as the market re-rates AI platform companies. That represents a 75% -120% return, not 10x. A true 10x requires either a dramatic re-acceleration in growth or a decade of sustained compounding near current rates. Neither is impossible. Both require strong execution.

5-Point Investor Takeaway

1. Core strength: Workflow data gravity and platform lock-in across the Global 2000. The deeper ServiceNow embeds into an enterprise’s operations, the harder it is to remove.

2. Key dependency: Revenue growth staying above 18-20% annually. If the company decelerates below that threshold, the multiple compression from today’s level would be severe.

3. Top growth driver: AI agent monetization via the hybrid consumption model. If enterprises replace headcount with AI agents running on ServiceNow, the total addressable market expands dramatically even as seat count compresses.

4. Main risk: Seat-based compression without adequate hybrid revenue offset. If AI agents reduce human users faster than consumption revenue scales, there will be a painful transition period.

5. Biggest unknown: How fast Moveworks, Veza, and Armis integrate and contribute meaningfully to revenue. These are AI-native, pre-revenue-scale businesses. The execution risk of three simultaneous integrations is real.

Bull & Bear Case Scenarios

The bear case here is not a disaster. Even if growth slows, the free cash flow profile limits the downside relative to where this stock was a year ago. The real risk is dead-money territory near today’s price if the market refuses to re-rate until AI monetization is clearly visible in results.

The bull case is genuinely exciting. A 25% grower running 40% free cash flow margins with three AI-native acquisitions coming online and a clear seat-plus-consumption pricing evolution deserves a premium multiple. The path back to $200-250 is cleaner than most people think right now because sentiment is so negative.

ServiceNow at $113 is a much better setup than ServiceNow at $239. The business has not gotten worse. The story has gotten bigger, the execution has stayed on track, and the stock is down 53% from its high. For patient investors with a 3-5 year horizon, the asymmetry here looks interesting. I am not saying it is cheap by traditional metrics. But high-quality compounders rarely are.