PORTFOLIO UPDATE +218%

Earnings Reviews from NBIS, IREN, MELI, PRM

Happy Sunday,

This is the weekend update, designed to give you everything you need to stay informed in under 5 minutes so you can get back to your weekend.

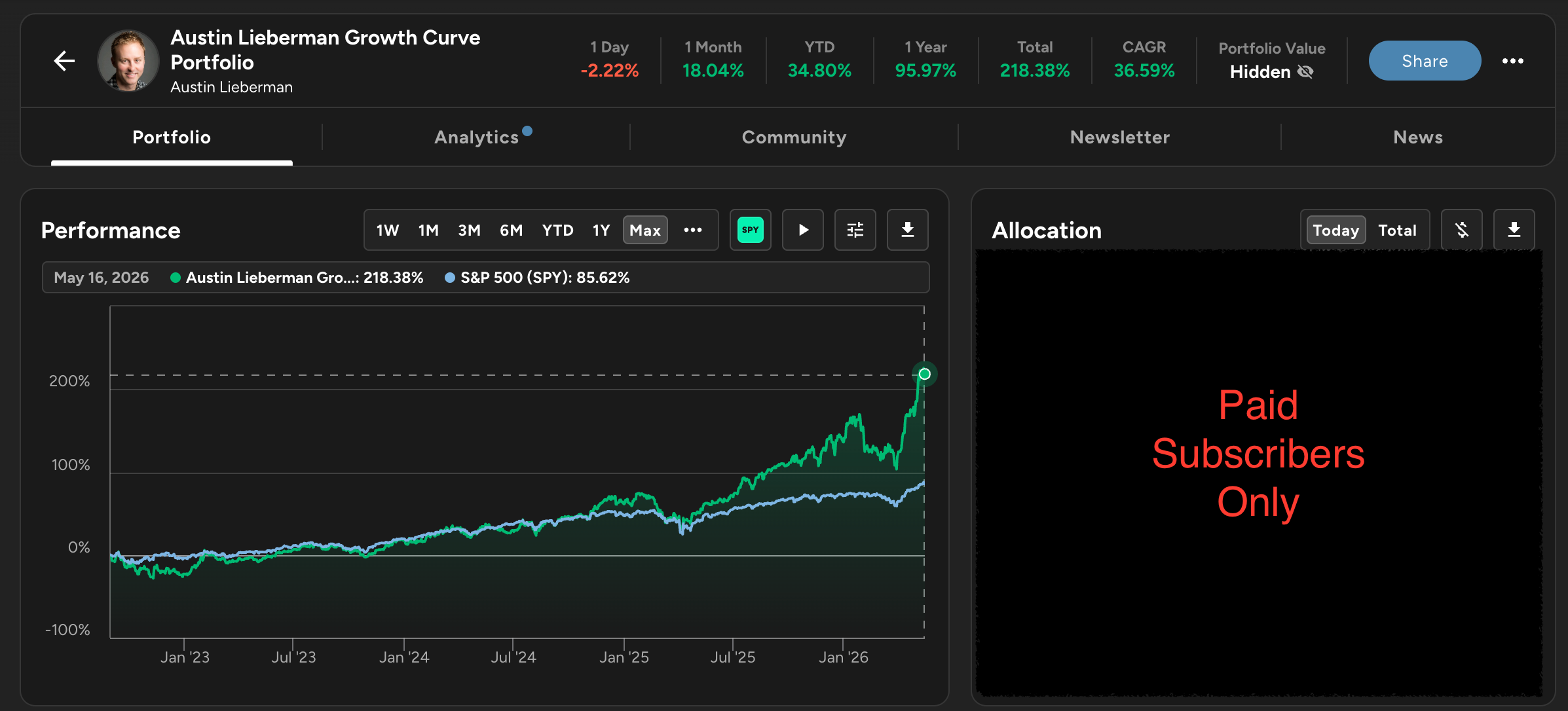

The portfolio closed Friday up 218% since August 2022, compared with the S&P 500’s 86% over the same period.

The lifetime numbers as of Friday’s close:

Total return since inception: +218%

CAGR: 37%

1-year return: +96%

1-month return: +18%

YTD return: +35%

S&P 500 over the same period since inception: +86%

That’s roughly 133 percentage points of cumulative outperformance vs. the index. Friday was a rough day for the broader market (S&P -1%, Nasdaq -2%, Russell 2000 -2%) and the portfolio took a hit alongside it at -2%.

Our focus in today’s newsletter is to cover earnings from four of our companies: PRM, IREN, MELI, and NBIS.

What’s on Deck

ServiceNow (NOW) reports in the back half of May. I’ll preview the setup next before they report.

Also, I’m finalizing the Nu Holdings (NU) deep dive. The Q1 earnings on May 14 confirmed everything I wanted to see in the thesis. Subscribers will receive the full bull, base, and bear scenarios when I send the deep dive this week.

As always, reply to this email with questions or pushback. I read everything.

Have a great weekend.

Earnings Review: Perimeter Solutions (PRM)

Reported: Wednesday, May 6

Position size in portfolio: 9%

Closed Friday at: $33.23

My cost basis: $23.18 (started buying at $13, added multiple times since)

PRM is a fire safety and specialty chemicals company. It supplies fire retardants and suppressants to government agencies like CAL FIRE and the US Forest Service, and operates the specialty chemicals business that recently expanded with the Medical Manufacturing Technologies acquisition.

It’s also one of the most underfollowed names I own. You won’t see it on CNBC. It doesn’t get covered on Fintwit. And it just put up a quarter that genuinely surprised me to the upside.

The Numbers

Net sales of $125.1 million, up 74% year over year

Adjusted EBITDA of $41.2 million, up 128% year over year (more than doubled)

Net income of $72.9 million ($0.44 per diluted share)

Adjusted net income of $9.0 million ($0.06 adjusted EPS) vs. analyst consensus of a $0.13 loss

Fire Safety segment revenue of $45.4 million, up 22% YoY, with segment adjusted EBITDA nearly doubling to $18.7 million

Specialty Products segment revenue of $79.6 million, up 128% YoY (driven by acquisitions)

The revenue beat of 152% over the $49.68 million consensus is large in part because the Street wasn’t fully accounting for the Medical Manufacturing Technologies acquisition that closed in December 2025. Even adjusting for that, the underlying business outperformed.

The Two Contracts That Matter Most

The most important news in the print wasn’t the numbers. It was the two long-term contracts the company signed.

First, a $500 million suppressants agreement with the US Defense Logistics Agency. This is a multi-year contract that will progressively contribute revenue through 2028. The DLA is one of the largest single buyers of fire suppressants in the world. This is the kind of contract that turns a cyclical fire-season business into something much more predictable.

Second, a renewed five-year contract with CAL FIRE for retardants, featuring enhanced year-one pricing and escalators. CAL FIRE is the gold-standard customer in this space. Locking them in for five years at improved pricing is a major win.

CEO Haitham Khouri called these out on the earnings call as the reason the business now has “a durable and predictable earnings base.” That’s a meaningful change in the investment thesis. PRM has traditionally been viewed as a seasonal play tied to wildfire severity. The Street has had a hard time valuing it because of that. The shift toward long-term contracted revenue, similar to what we’ve seen with SNDK on the memory side, transforms how the multiple should be set.

Why I’ve Held This Position For So Long

I started buying PRM at $13. The stock is now $33.23, up roughly 156% from my first buys. I’ve added multiple times along the way, which is how the cost basis ended up at $23.18.

The thesis was always simple. Wildfires are getting worse, not better. Government budgets for fire suppression are growing. The supplier base is concentrated, and Perimeter is the dominant player in long-term retardants for the US and a growing player in international markets. The regulatory moat is real. The pricing power is real. And the management team, run by an investor-operator named Haitham Khouri, treats capital allocation seriously.

The Specialty Products side adds optionality. The MMT acquisition is the kind of thing that doesn’t show up cleanly in next-quarter numbers but compounds over time. Medical manufacturing is a specialty chemistry business with high margins and sticky customers. It diversifies away from the seasonality of the fire business without changing the core thesis.

What I’d Watch From Here

The stock declined 9% the day before the earnings release. I have no idea why. Sometimes the market does this. The earnings beat the next morning more than reversed it, and the stock is now trading near all-time highs.

The full-year analyst EPS estimate is $1.41. That’s likely to move higher as the Street folds the new contracts into models. Q2 is typically the seasonal peak for the fire safety business, so the next earnings report will tell us whether the operational momentum is sustainable.

PRM is an example I’d point to when someone asks what value Growth Curve Investing brings. There are dozens of small, underfollowed, well-run companies hiding in plain sight that don’t get the attention they deserve. Those are the hidden gems that can deliver outsized returns for many years and they’re exactly the type of company I look for and share in the newsletter.

The rest of this email, including the IREN, MELI, and NBIS earnings reviews and my full portfolio walkthrough, is for paid subscribers.