PORTFOLIO CHANGE: +260%

I'm raising the largest cash position I've had in years. Here's exactly what I'm doing and why.

Happy Friday,

This is the paid-only follow-up to yesterday’s email (link). I want to be direct with you. What I’m sharing today is a more meaningful shift in how I’m positioning the portfolio than what I initially planned, and I want to walk you through exactly why my thinking has evolved over the past several weeks.

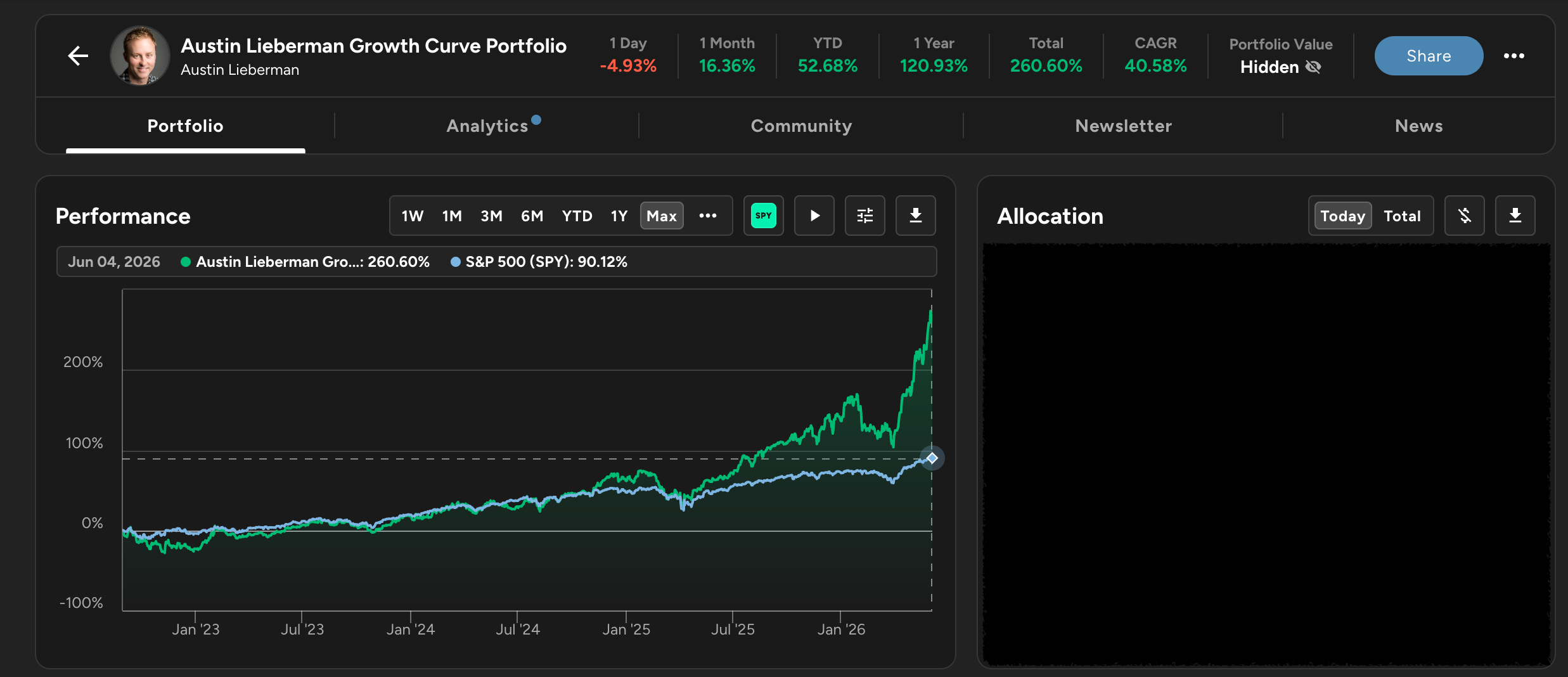

As of the close yesterday the portfolio is up 260% since August 2022 compared to a 90% return for the S&P 500. That is incredible and unsustainable performance.

It hasn’t just been my portfolio that is outperforming. I did benefit from concentrating heavily into stocks that have outperformed but the broader market has been performing better than normal as well.

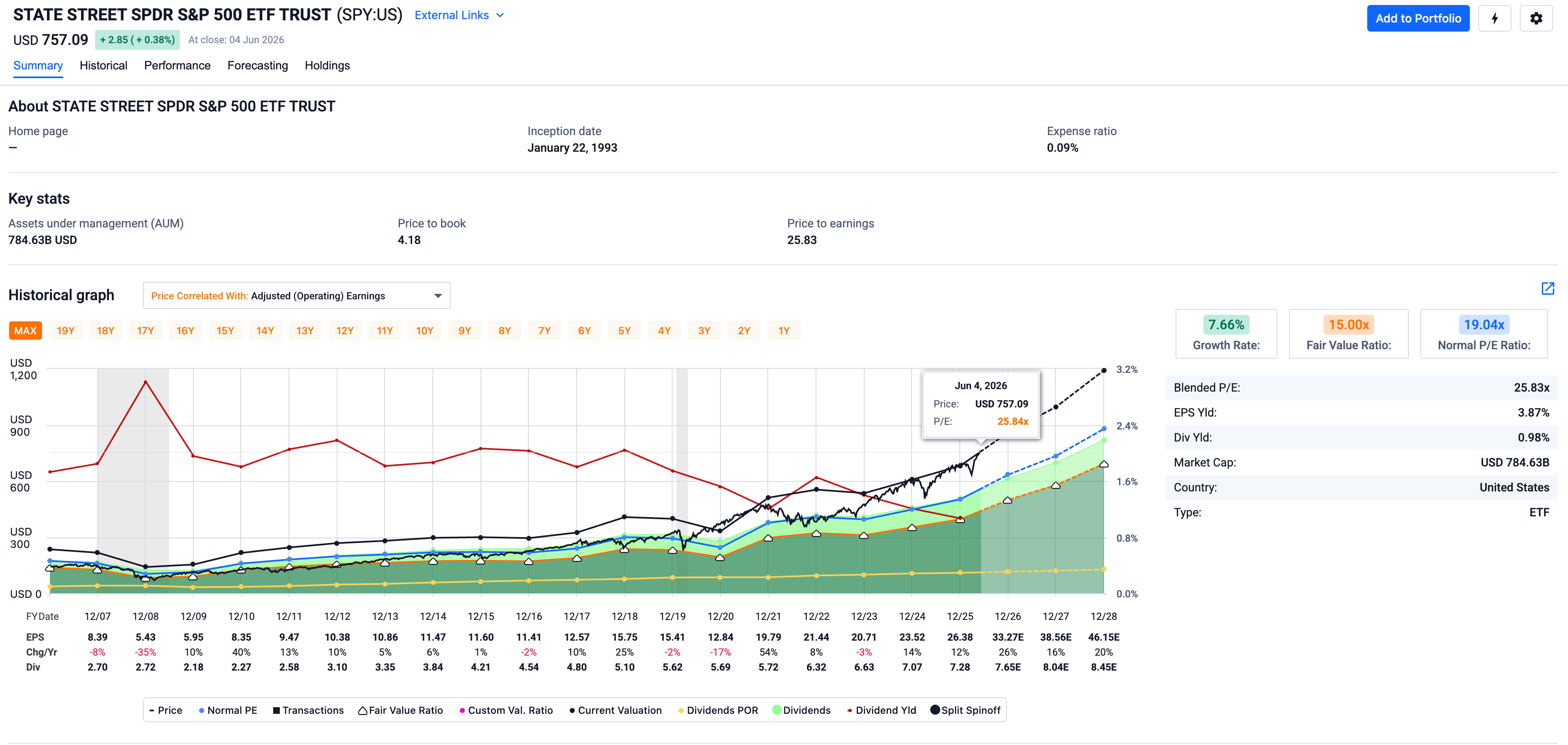

Here’s a look at the SPY which tracks the S&P 500. You’ll notice the current Blended P/E as calculated by FAST Graphs (my absolute favorite investing tool) is almost 26x compared to a normal P/E of 19 since 2006. That means it would take either accelerated earnings growth or a 27% pull back for the index to be back in line with its historical valuation.

I think it is more likely we have a deceleration in earnings instead of an acceleration because expectations are so high and so I believe it’s more likely we see a 20% - 30% pullback than continued outperformance.

With that in mind, this is a portfolio of individual stocks, not just the SPY but if the broader market pulls back, some of the higher volatility stocks that we have beenefitted from owning will pull back even more.

I want to be clear, I’m not becoming a perma-bear and I’m not trying to fear monger. If I was just beginning investing and my portfolio contributions were 20% or more of my portfolio value per year, I probably wouldn’t make any changes.

But I’m not at that stage anymore because I’ve been building the portfolio for a while and my contributions don’t have a big impact on the portfolio value.

I can’t tell you what to do with your own portfolio; that’s a decision only you can make, and everyone’s situation is different. But what I’m trying to do with my portfolio and this newsletter is share my process and try to beat the market/make money over the long-term.

With all of that being said, here’s exactly what I’m going to do and why. I’ll share my positions allocations and what the full portfolio will be after these trades are done towards the end of this email.

Sell 100% of NBIS (currently 16% of the portfolio)

Sell 100% of IREN (currently 11% of the portfolio)

Trim SNDK from 23% to 8%

Hold MU at its current 8%

That is approximately 45 percentage points of capital coming out of AI infrastructure and AI memory positions. After the trades, the portfolio will hold around 45% cash. I expect to deploy that cash methodically over the coming weeks and months into high-quality, undervalued companies that I am actively researching now.

The underlying businesses at NBIS and IREN are real. The contracted backlogs are real. The execution to date has been impressive. I am not selling because I think these are bad businesses. I am selling because I believe current stock prices require near-perfect execution over multiple years to justify the valuations, and the path to that execution requires substantial additional capital raises that will dilute existing shareholders. The asymmetry no longer favors holding the positions.

Here’s why I feel that way

The Macro Setup: Hyperscaler Capex Has Outrun the Revenue

Start with the broader AI infrastructure capex picture. Hyperscaler capital spending in 2026 is on track to reach $725 billion or higher. Morgan Stanley published a note earlier this year framing this build-out as larger in magnitude and longer in duration than the telecom infrastructure boom that preceded the dot-com bust. Their analysis suggests hyperscalers will drive roughly 40% of total Russell 1000 cash capex over 2026 to 2028, which is more than $2 trillion of spending concentrated in a handful of companies.