Nu Holdings Deep Dive

PORTFOLIO: +268%. Updates on MU, SNDK, NBIS, IREN

Happy Thursday,

Two emails going out this week. This one is for every subscriber, free and paid. It covers the latest portfolio performance and the full Nu Holdings (NU) deep dive I’ve been working on for several weeks.

The second email goes out tomorrow morning to paid subscribers only. It will have the full portfolio walkthrough with every position, plus a refreshed look at the bull and bear scenarios for the four AI-memory and infrastructure names that have driven most of the recent gains: MU, SNDK, IREN, and NBIS.

Portfolio Performance Update

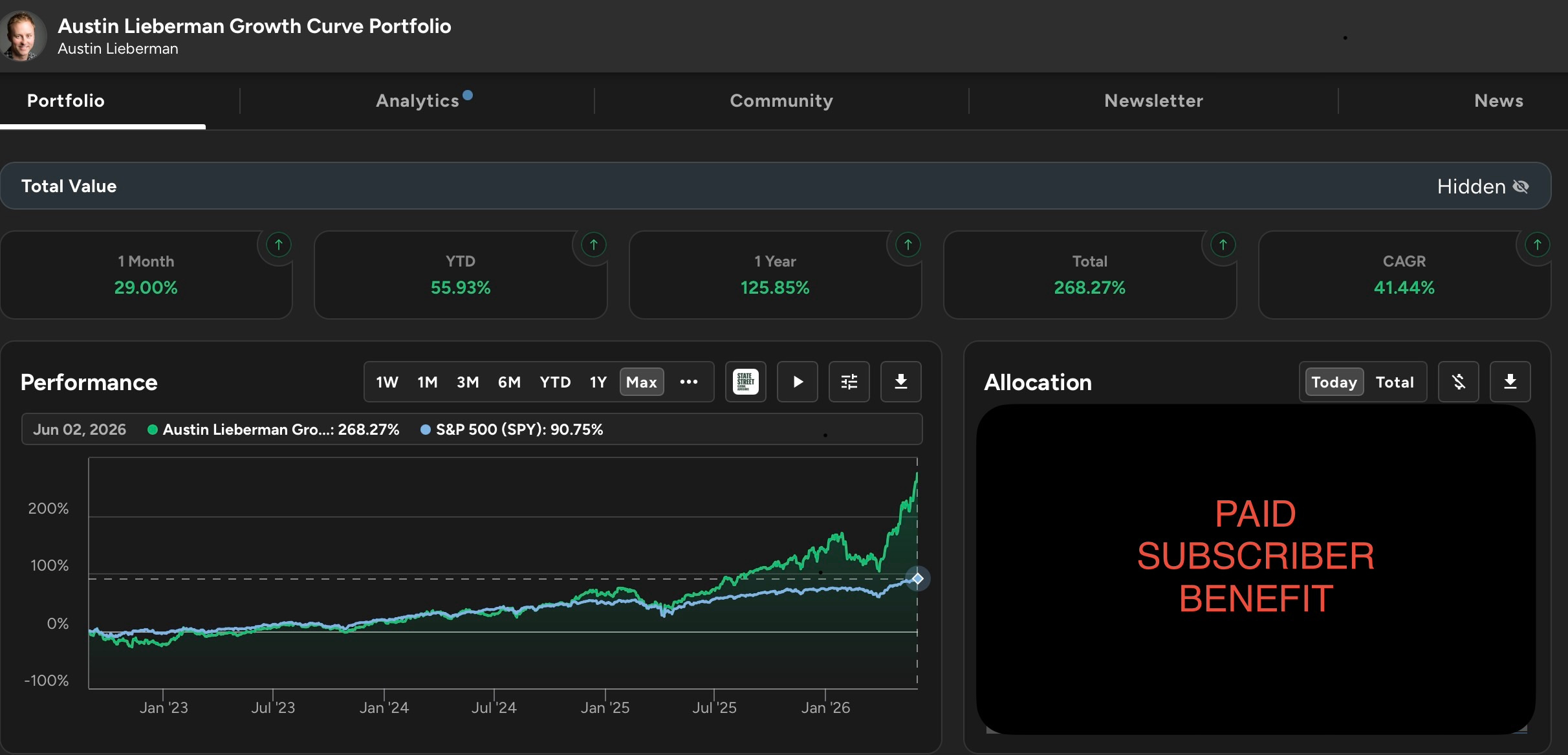

The portfolio closed Monday up 268% since August 2022 (when I started tracking using SavvyTrader) against the S&P 500’s 91% over the same period. The numbers as of yesterday’s close:

Total return since inception: +268%

CAGR: 41%

1-year return: +126%

YTD return: +56%

1-month return: +29%

S&P 500 over the same period since inception: +91%

That’s roughly 177 percentage points of cumulative outperformance vs. the index.

I want to be honest about something. This is the third consecutive month of 25%+ returns. These kinds of returns are not sustainable and I do not expect them to continue at this rate. Memory and AI infrastructure stocks have been the dominant drivers, and that part of the market has not seen a meaningful drawdown in months.

There will be a pullback at some point which isn’t a reason to be afraid or avoid the market completely, but now is a great time to make sure you are not taking on too much risk or have too much of your portfolio in any single stock or sector.

I can’t tell you the exact percentage, but in general, 15% in a single stock or 25% in a single sector is a good rule of thumb.

What I will say is that the underlying businesses in the portfolio continue to execute, and in several cases, accelerate. The numbers are real. The earnings power is real. The contracted revenue backlogs are real (though in a severe downturn, customers could back out).

Whether the multiples hold through normal near-term volatility is the open question.

The full position-level breakdown, including how I’m thinking about sizing across the names that have run hardest, is in tomorrow’s paid email.

The Full Nu Holdings (NU) Deep Dive

Nu Holdings reported Q1 2026 on May 14 and delivered the strongest quarter in company history. The market initially yawned. Then it sold off. Then on Monday the company announced a planned CFO transition. Then Bank of America downgraded the stock to Underperform this morning and cut its price target. The shares are trading around $11.93 as I write this, down 7% on the day, down 37% from the all-time high of $18.98 set on January 29.

This is exactly the kind of setup I look for. A high-quality business executing on plan, hated by sentiment, mispriced by short-term concerns the market is overweighting, and largely ignored by US investors who don’t follow Latin American financial services. Let me walk you through why I think NU is one of the most attractive opportunities in the market right now.

The Business

Nu Holdings is the parent of Nubank, the largest digital bank in Latin America. The company was founded in 2013 by David Vélez (still the CEO) with a single product: a no-fee, no-branch credit card aimed at Brazilian consumers who had been historically underserved by the traditional banking oligopoly.

Thirteen years later, the company has 135 million customers across Brazil, Mexico, and Colombia. To put that number in context, Brazil’s total adult population is roughly 165 million. Nubank has roughly 60% of all Brazilian adults as customers. In Mexico, the company crossed 15 million customers in Q1 and became the third-largest financial institution in the market. In Colombia, the customer base is approaching 5 million.

Nu is not just a bank. The company offers credit cards, personal loans, savings accounts, investment products, payments, insurance brokerage, life insurance, and a fast-growing marketplace product. The business model is built around a flywheel: get the customer in with a great product (originally the credit card, now often the no-fee bank account), monetize them through cross-sell over time, and operate the whole thing at a fraction of the cost-per-customer of incumbent banks.

The result is one of the most efficient banking operations on the planet. Cost-to-serve per customer is roughly $4 per month, against more than $35 per customer for the average traditional Brazilian bank.

The Q1 2026 Numbers

This was a record quarter on essentially every metric the company tracks. The full numbers from the Q1 2026 release, filed with the SEC on May 14:

Revenue of $5.3 billion (record), surpassing $5 billion for the first time

Net income of $871 million, up 56% year over year on an FX-neutral basis

Return on equity of 29%

Efficiency ratio of 17.6%, a record low

4 million new customers added in the quarter

Consolidated credit portfolio of $37.2 billion, up 40% YoY FX-neutral

Mexico achieved business break-even

AI transformation reached 15 million monthly active users on Nubank AI features

For context on the efficiency ratio: most US large-cap banks operate with efficiency ratios in the 55% to 65% range. JPMorgan’s was 55% in 2025. Bank of America’s was 64%. Nubank at 17.6% means the company spends 17.6 cents on operating expenses for every dollar of net interest income and fee revenue. That is not a banking number. That is a software company number.

The Three-Country Story

What makes Nu different from other “fast-growing emerging market bank” stories is that the same playbook has now worked in three different countries, each at different stages.

Brazil is the mature market. 115 million customers, the largest private financial institution in the country by customer count, and still growing. Brazil ARPAC (average revenue per active customer) was $11.20 per month in Q1, up from $9.40 a year ago. Even at scale, the company is taking share from the incumbent banks (Itaú, Bradesco, Banco do Brasil, Santander Brasil) on basically every product line.

Mexico is where the leverage shows up. Nu has 15 million customers in Mexico, up from 6.6 million in Q1 2024 and 2.1 million in Q1 2022. The business achieved break-even in Q1 2026. The efficiency ratio in Mexico has dropped from 120% in Q1 2022 to 42% in Q1 2026, a 78-percentage-point improvement in four years. Mexico ARPAC is now $12.40 per month, higher than Brazil’s $11.20 (an important data point that we’ll come back to).

Colombia is the early-stage opportunity. Roughly 5 million customers and growing. The trajectory looks like Mexico’s did four years ago.

The thesis I’d offer is this: if you believe the Brazil playbook can be replicated in Mexico, and the Mexico playbook can be replicated in Colombia, and the company can continue to compound at the customer-acquisition and ARPAC expansion rates it has demonstrated, then NU at today’s price is dramatically underpriced. The Mexico ARPAC being higher than Brazil’s at much earlier scale is the single most important data point in the company’s whole story. It tells you the model works better as the company moves into wealthier markets with deeper financial inequality.

The US Banking Approval

In January 2026, Nubank received conditional approval from US regulators to operate a US national bank. This is the wild card in the long-term thesis.

The company has been deliberately quiet about the US strategy. The most we know is that the target is initially the underserved Latino population in the US (roughly 65 million people, with high remittance flows back to Latin America that Nu is uniquely positioned to capture).

I am not modeling significant US revenue contribution in the next three years. But if Nubank can execute on the US opportunity even half as well as they’ve executed on Mexico, the upside is enormous. The US ARPAC potential is many multiples of the Brazil and Mexico ARPACs.

The AI Transformation

The other piece of the story that doesn’t get enough attention is what Nu is doing internally with AI. CEO David Vélez spent a meaningful portion of the Q1 2026 shareholder letter on it. The framing is “we are not adding AI to banking, we are rebuilding banking around AI.”

The data points the company shared in the most recent results:

Engineering throughput up 50% year over year

Weekly token consumption inside the company nearly 10x higher than at the start of 2026

Testing cycles 90% faster

15 million monthly active users on Nubank AI features inside the app

Proprietary credit underwriting models are now in production

Nu has roughly 10,000 employees serving 135 million customers. That is approximately 13,500 customers per employee. The closest comparable in the US is JPMorgan Chase at roughly 240 customers per employee. The AI transformation should widen that operational efficiency gap meaningfully over the next several years.

Why The Stock Is Down 37% From All-Time Highs

This is the question investors are asking right now. The answer is a combination of three things, none of which are thesis-breaking.

First, Brazilian credit normalization. After several years of aggressive credit expansion and low default rates, Brazilian credit losses are normalizing in 2026. This is happening across every Brazilian bank, not just Nu. Bank of America’s downgrade this morning cited “FY26 and FY27 net income estimate cuts of 6% and 9% respectively” tied to higher credit provisioning. That is a real concern but it is not catastrophic, and Nu’s risk management has held up well in similar credit cycles in the past.

Second, the CFO transition. On June 1, Nu announced that long-time CFO Guilherme Lago is moving to a Special Advisor role and will be replaced by Rob Livingston, formerly CFO of Visa North America. Livingston starts July 13. Lago stays on through August 31 to support the transition. The market does not love unexpected CFO changes. The market especially does not love them when they are announced one quarter after a slight EPS miss. The company has been clear that this is a planned, orderly transition that does not change the operating model, risk appetite, or long-term strategy. I take them at their word, particularly given that Livingston is a meaningful upgrade in international finance and payments experience.

Third, the slight Q1 EPS miss. Reported EPS of $0.18 came in below the $0.20 consensus estimate (the company doesn’t formally guide). The revenue beat ($5.32B vs. $5.06B consensus) and the strong operating metrics got drowned out by the EPS miss in the immediate market reaction.

All three of these are real but recoverable concerns. None changes the business's fundamental compounding profile.

The Bull / Base / Bear Cases

Here’s my 3-year framework. Anchored to today’s price of around $11.93 (NU does not have a fiscal year that lines up with calendar years cleanly, so I’m using calendar 2028 as the horizon).

Bear case. Brazilian credit cycle deepens, Mexico growth stalls, US delays drag on. I model 2028 EPS of $0.85 against a compressed 14x multiple, which gets to $11.90 per share. Essentially flat from today.

Base case. Brazil compounds at low-teens YoY, Mexico continues scaling, and the US begins contributing. 2028 EPS of $1.20 at 20x equals $24.00, which is +101% over three years (roughly 26% CAGR).

Bull case. All three markets compound at strong rates and the US ramps faster than the consensus expects. 2028 EPS of $1.65 at 25x gets to $41.25, or +246%.

Mega-bull. International expansion accelerates beyond Mexico and Colombia, and AI transformation drives meaningful margin expansion. 2028 EPS of $2.10 at 28x equals $58.80, or +393%.

The base case implies the stock essentially doubles over three years. That’s a 26% CAGR, which is not crazy for a company growing earnings at 30-40% annually with a real competitive moat. The bull case implies a triple. The mega-bull implies a quadruple-plus.

The bear case is the most interesting one to me. Even in a scenario where the Brazilian credit cycle keeps biting, Mexico growth stalls, and the US opportunity gets delayed, the stock is essentially flat from here. That’s a powerful asymmetry. The downside is not zero (no stock’s downside is ever zero), but the floor looks much firmer than many growth stocks that have run so much higher recently due to AI hype.

Risks

Three risks worth flagging.

Brazilian macro and currency. The largest revenue contributor is Brazil. If the Brazilian real depreciates significantly against the US dollar, USD-reported results compress regardless of operational performance. Nubank reports growth rates on an FX-neutral basis to help investors see through this, but the headline numbers can disappoint.

Credit cycle. Nubank’s credit portfolio is up 40% year over year. That’s aggressive growth in a market that is normalizing. If the credit cycle deepens further in 2026 or 2027, provision expenses will weigh on earnings. The company has shown disciplined underwriting historically, but the current pace of credit growth is the most aggressive in the company’s history.

Competitive pressure. The Brazilian incumbent banks (Itaú in particular) have improved their digital offerings significantly. Nu’s growth in Brazil from here has to come from share gains in higher-income segments, where the competitive pressure is stronger than in the underbanked segment Nu originally targeted.

My Position and Sizing

Paid subscribers will be the first to know if I open a position and my allocation percentage, if so.

Would I own NU and MELI?

If you believe (as I do) that Latin American fintech is structurally underrated by Wall Street because of currency and macro noise, owning both companies gives you exposure to the theme through two different operational angles. MELI tends to outperform when the market is paying for growth optionality. NU tends to outperform when the market is paying for cash flow compounding. The combination is durable.

What’s on Deck

The paid-only email tomorrow morning will have the full portfolio breakdown and refreshed bull/bear scenarios on MU, SNDK, IREN, and NBIS. All four have moved significantly since the last time I published scenarios, and the underlying numbers have changed in ways that materially affect how I’m thinking about sizing.

ServiceNow (NOW) reports in roughly three weeks. I’ll preview the setup in next week’s letter.

As always, reply to this email with questions or pushback. I read everything.