New Position: Cloudflare (NET)

Strong results, a bright future, and a valuation I'm comfortable with

I want to make this clear. I’m not in the game of timing bottoms or predicting what happens over the next 6 months.

On a recent podcast, David Gardner says three years is the shortest amount of time that we can truly judge investment performance and I agree.

That isn’t an excuse for being completely blind to excessive valuations which I (and many others) admittedly were for parts of the last couple of years.

I personally believe now if a great opportunity to be buying shares of great companies if your time horizon is 3+ years. That’s what I’m doing with my own money. I may be early and the market may fall a lot more….I truly have no idea.

But I’m finding reasonable multiples in many high-quality companies with mission-critical products, high gross margins, recurring revenues, high net-dollar-retention rates which indicate their customers find value in their offerings and keep spending more.

Those are the companies I want to find, buy, and own (as long as the business keeps executing and management demonstrates excellence) for the next 3, 5, and 10+ years.

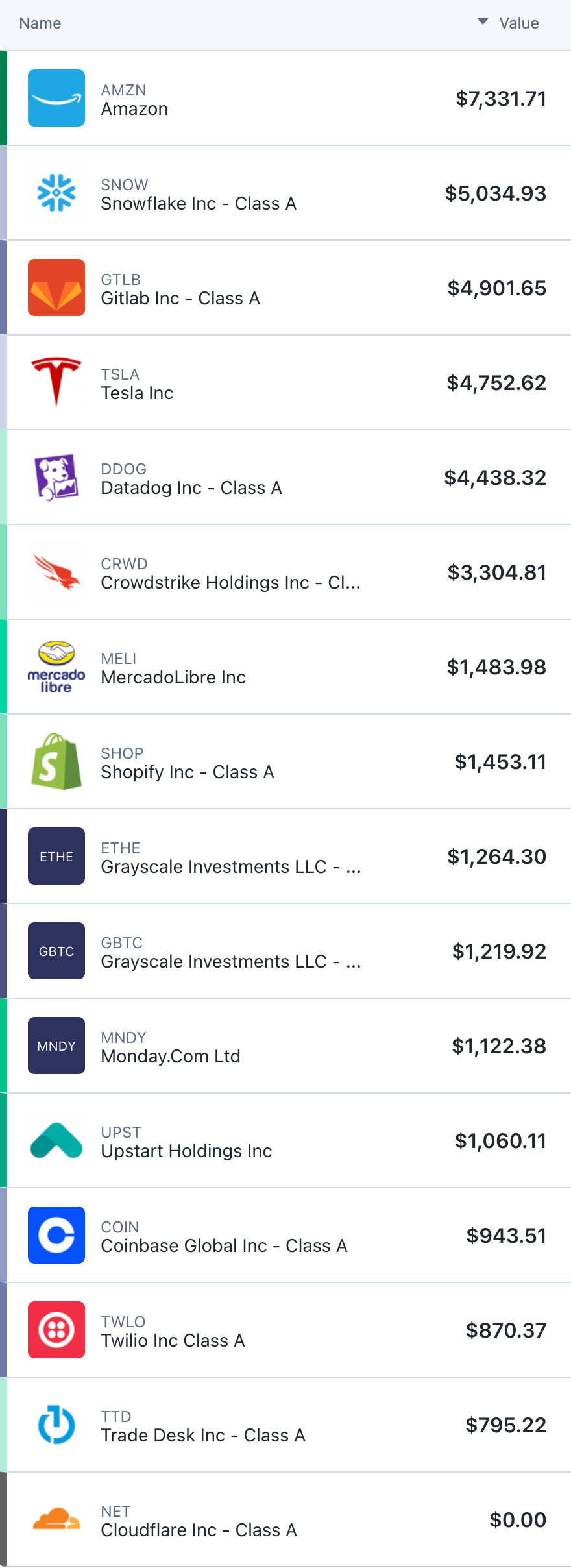

Here are all of the companies I currently own in the 2032 portfolio. Reminder, I intend to add to this portfolio every two weeks until 2032 or until we all lose our jobs in the coming doomsday depression that everyone is predicting (jk, I hope).

Why I’m buying Cloudflare (NET)

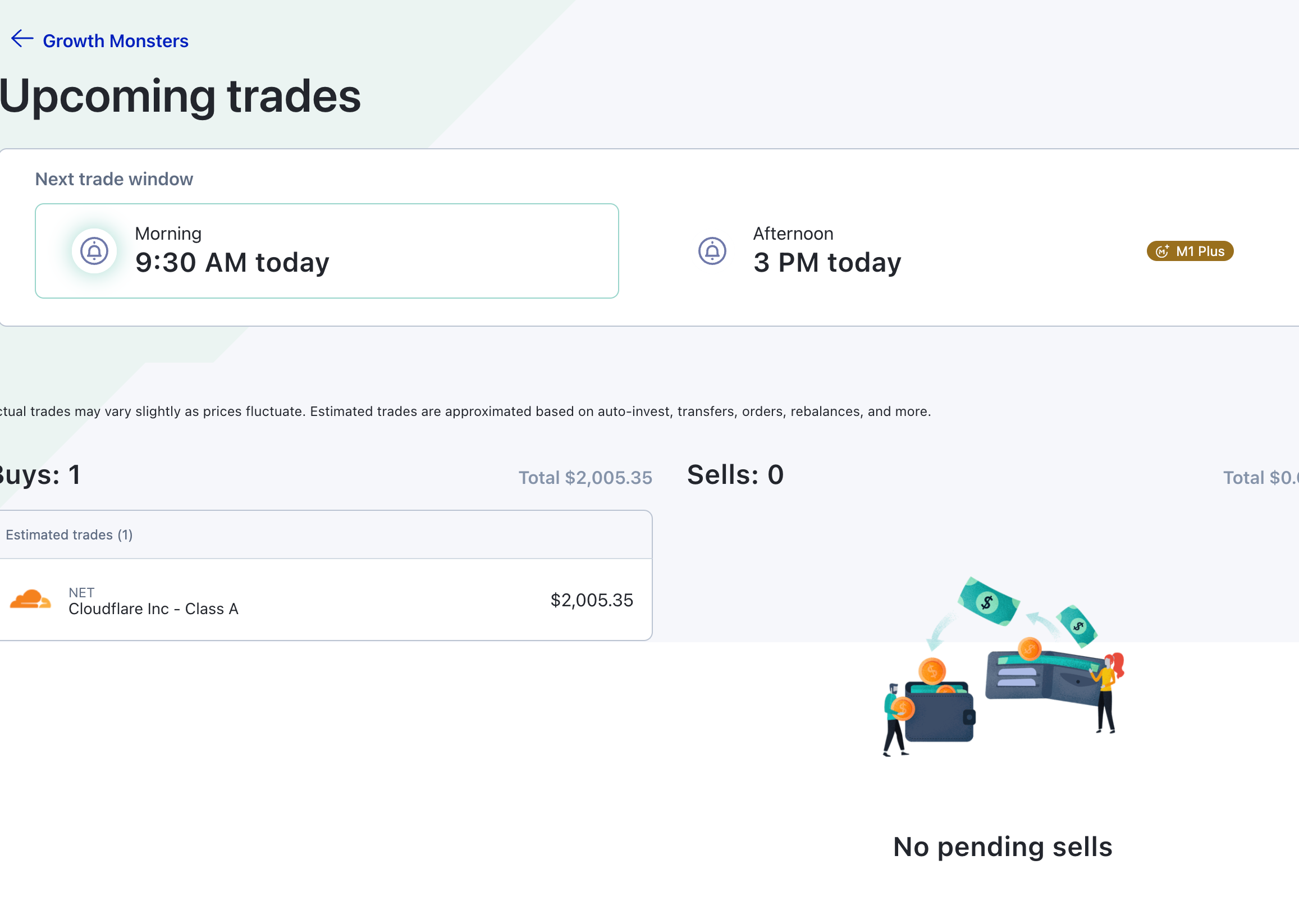

I’ll be buying $2,000 of Cloudflare this morning sometime between 9:30 EST and 10:30 EST.

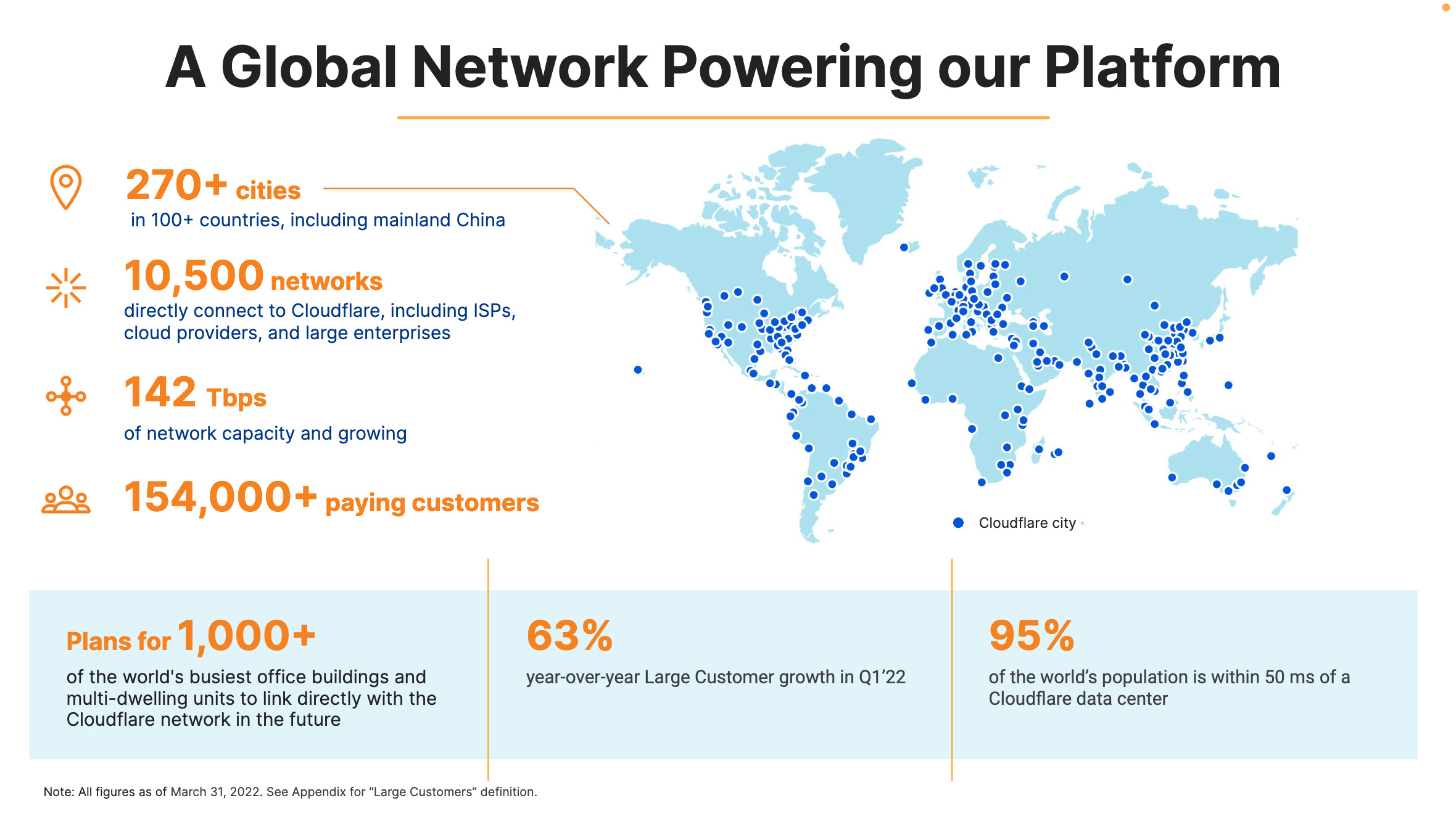

Cloudflare serves more than 154,000 paying customers with 47% of revenue coming from outside the U.S. No customer represents more than 5% of annual revenue so revenue is fairly diversified.

This is by no means a deep dive into the business… I’ll do that at some point. But I’m sharing this next slide to emphasize an important point. Cloudflare’s business requires far more CapEx than SaaS businesses like Datadog, Atlassian, and others.

That can be seen as a disadvantage in terms of whether or not Cloudflare deserves the same type of multiple as a Datadog, but also a potential advantage because it’s theoretically harder for a competitor to replicate Cloudflare’s approach due to the high costs and lead Cloudflare has in building out its network.