Investment Ideas: Deloitte's Technology Fast 500 Pt 1

Searching the fastest growing companies in North America for investment ideas...

This is part 1 of 2…or maybe 3. But this is definitely part 1.

In part 1 we will cover Mohnish Pabrai and the inspiration for researching Deloitte’s Technology Fast 500 2019 list fo investment ideas and all the public companies on that list.

In part 2 we will cover the criteria I’m considering and my method for filtering companies out of the list (not interested in investing)

In part 3 we will cover whatever we don’t get to in part 2.

Mohnish Pabrai is one of the best investors around. The video below is a talk he did at Google. I had a bunch of takeaways from this talk - I’ll cover all of them in an email sometime.

There’s a couple I’ll summarize here because they led me to spend a bunch of time searching Deloitte’s list of the fastest-growing companies in North America from 2015-2018 for investment ideas…

Monish talked about some team at some fund (yeah I’m super technical) who thought they’d generate world-smashing returns if their analysts of great investors all picked only their best idea. Supposedly they did this multiple times and each time it not only failed to beat the S&P 500, but the returns were terrible.

Monish summarized that often times, people’s “best ideas” aren’t necessarily their best ideas. They are the ideas they have spent the most time thinking about. So there’s some type of sunk cost mentality associated with spending too much time focused on companies. We get emotionally tied to them and want them to be our best ideas. I’ve witnessed myself doing this. Have you?

He then talked about how he and Charlie Munger (and maybe Warren Buffett) want to see as many stock ideas as possible because they can say no to something like 99% of them in 30 seconds to 1 minute. He calls it being unreasonably picky when it comes to investments. Set standards and don’t lower them.

The scary thing about saying no so fast is the “what if” factor. That’s a very technical term. He didn’t say that, but it’s how it makes sense to me. Basically, this is the fear of something we pass up going up 10x or 100x. That is going to happen and it doesn’t hurt us if we’re not invested in it. We need to stick to our circle of competence (back to saying no fast) because we can be hurt by what we are invested in. Especially if we don’t understand it.

For me, this means avoiding most/all Pharma and Biotech companies.

Finally, he said something super insightful (turns out he’s kind of smart). He said he has had the fortune of having more than his fair share of 100-baggers (meaning 100x returners) in his portfolio, but he’s been too dumb to hold most of them.

For me, this comes back to owning companies we are comfortable with. If we’re not comfortable with a company we won’t hold onto it for that 10x gain so what’s the point of owning it?

He emphasized the importance of looking for companies with excellent moats, excellent management, and tail-winds behind the business. When you find one, two, or all three of those attributes, you have likely found a massive compounder.

When you find a compounder, DON’T SELL IT if it’s fairly valued or even over valued. Accordiny to Monish, you should only sell compounders if they are egregiously valued (that means really crazily valued).

5. He also said if we’re in our earning years with 10-20 years of earning and adding to our investments ahead of us, it probably doesn’t make sense to own more than 10-12 companies.

Okay so I basically just summarized my Mohnish Pabrai points…. I just saved you another email. But here is a really important point. He’s one of the greatest investors around. So are Warren Buffett and Charlie Munger. But I won’t apply all of their rules. It’s not because I think I’m smarter than them. It’s because I’m not them. I have a different temperament. Different investing experience, a different outlook on investing, life, family, etc.

So I’ll figure out what works for me and try it out.

Onto the Deloitte list. Here’s a link to the list on Deloitte’s site.

First, what does it take to make this special list? Don’t ask me, ask Deloitte.

Selection and qualifying criteria Technology Fast 500 provides a ranking of the fastest-growing technology, media, telecommunications, life sciences, and energy tech companies—both public and private—in North America. Technology Fast 500 award winners for 2019 are selected based on percentage fiscal year revenue growth during the period from 2015 to 2018. In order to be eligible for Technology Fast 500 recognition, companies must own proprietary intellectual property or technology that is sold to customers in products that contribute to a majority of the company’s operating revenues. Companies must have base-year operating revenues of at least $50,000 USD, and current-year operating revenues of at least $5 million USD. Additionally, companies must be in business for a minimum of four years, and be headquartered within North America. This ranking is compiled from nominations submitted directly to the Technology Fast 500 website, and public company database research conducted by Deloitte LLP.

Some takeaways.

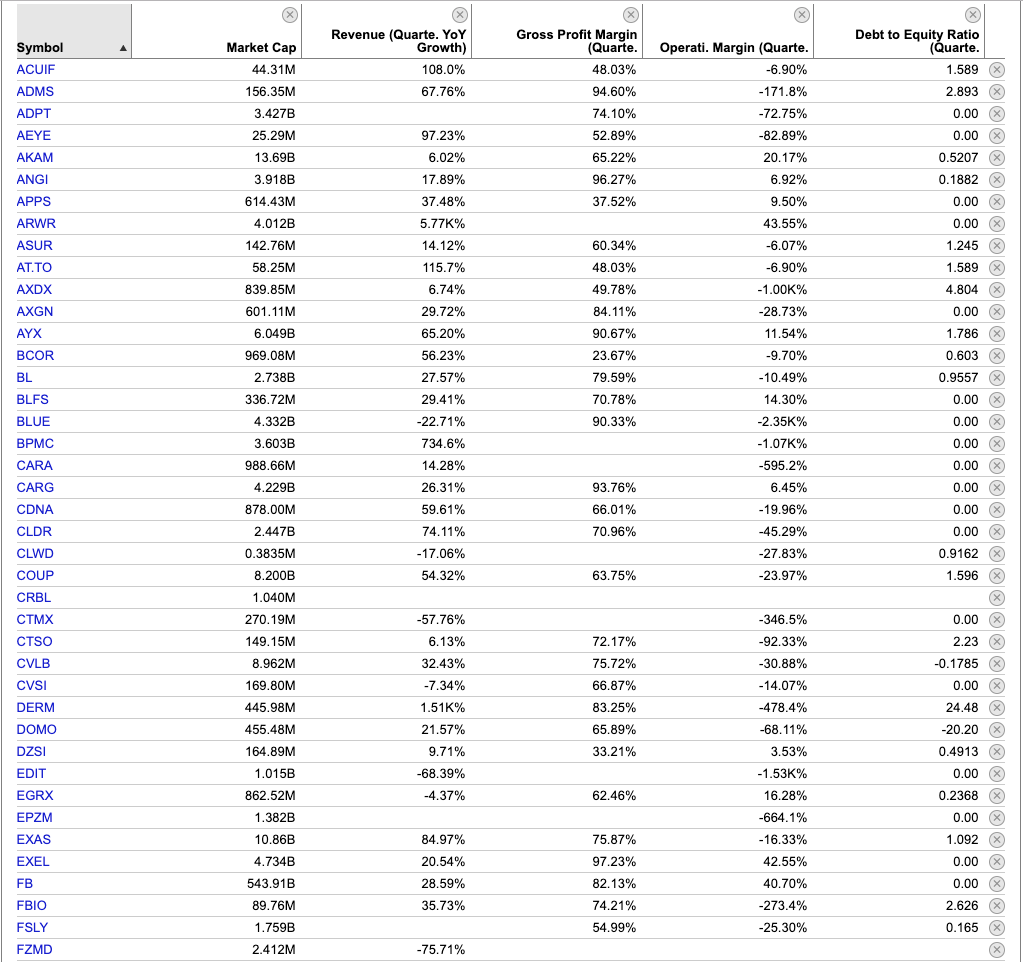

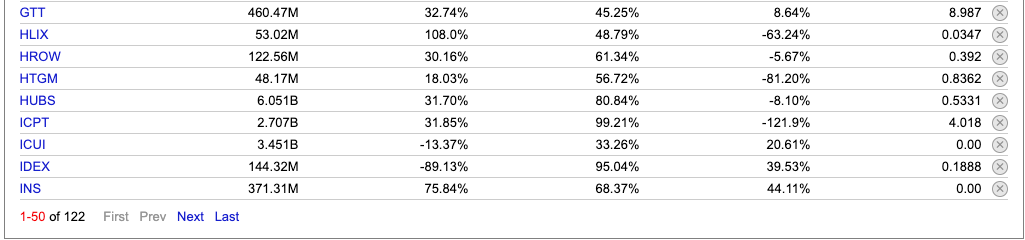

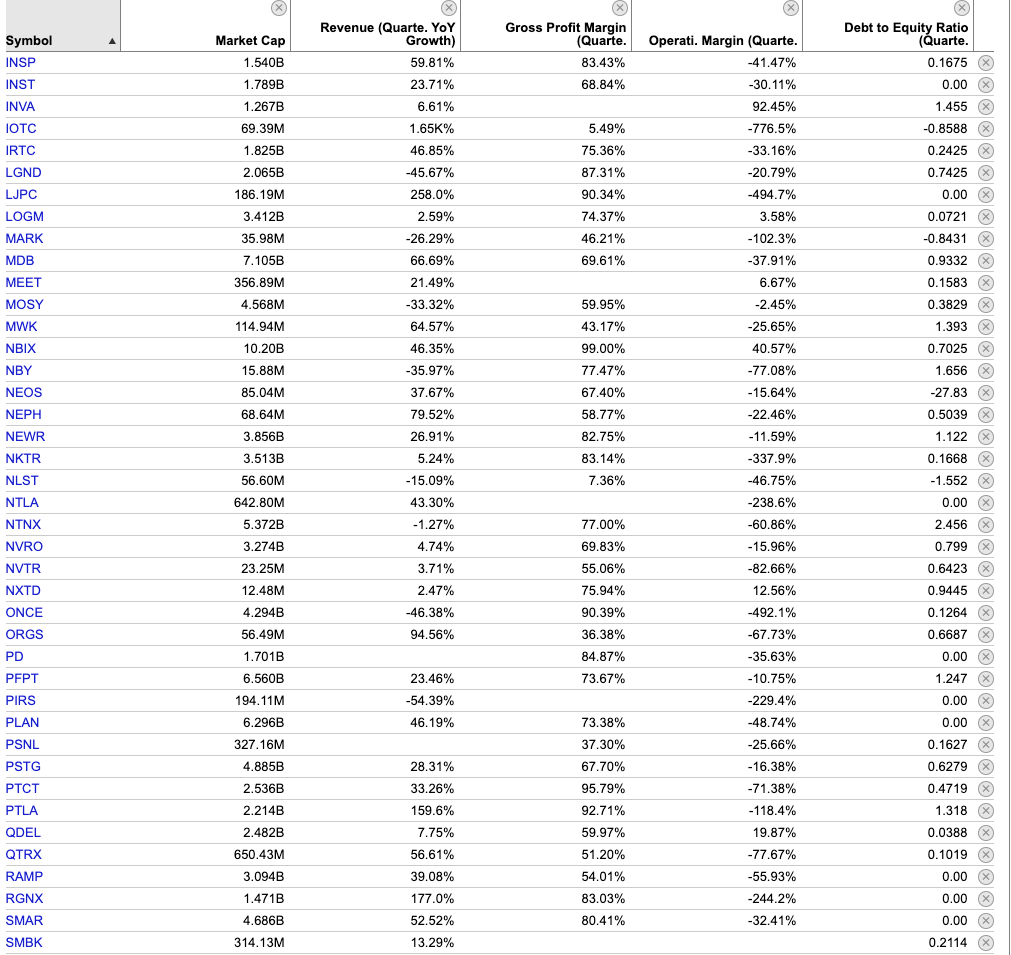

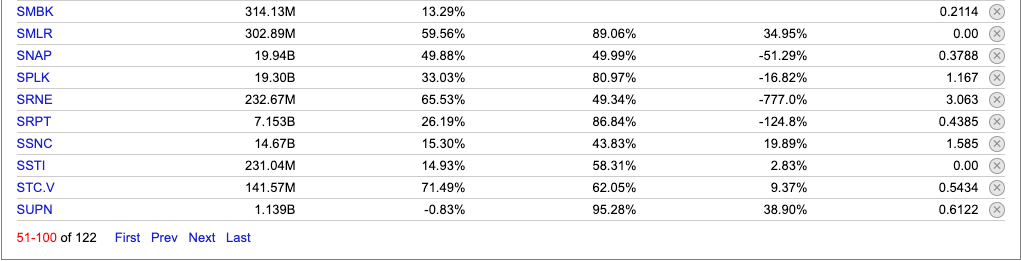

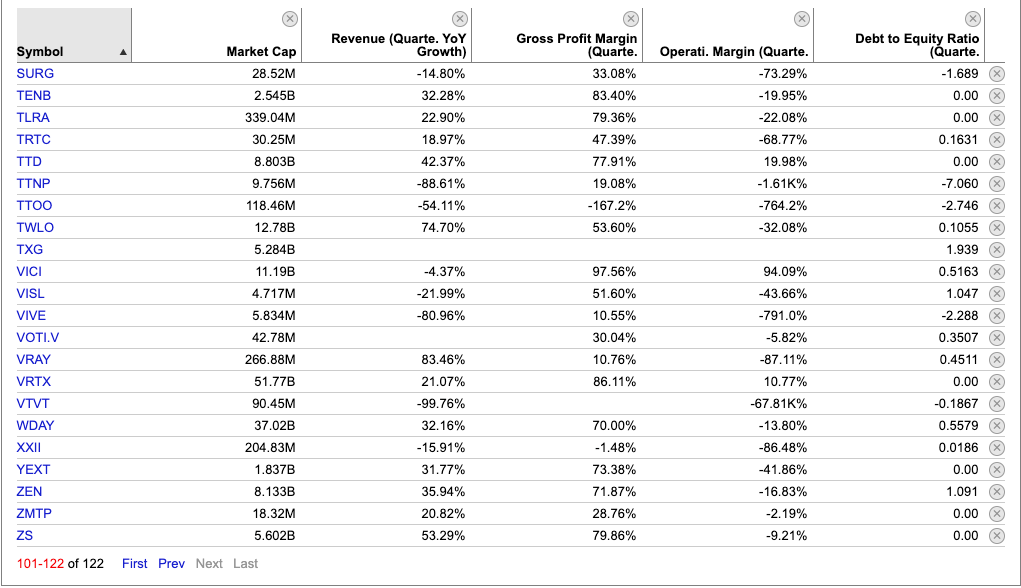

122 of the 500 companies on the list are public

Most of them are Pharmaceutical or Biotech companies. I will likely eliminate most or all of those.

The highest YoY revenue growth is Arrowhead Pharmaceuticals Inc (ARWR) at 5,077%. The share price is up 147% in 1yr, 45% in 5 yrs, -3.83% in 10 yrs, and -10.42% in 20 yrs.

The lowest YoY revenue growth is vTv Therapeutics (VTVT) clocking in at -99.76%. The share price is down 48% in 1yr and down 34% in 3yrs. (maybe this one isn’t actually on the list… I dunno.

The smallest market cap company on the list is Netlist (NLST) with a market cap of $56M

The largest market cap company on the list is Facebook (FB) with a market cap of $543B

Many companies I currently own are on this list: AYX, EXAS, NBIX, PD, PLAN, TTD, ZS

Finally, the list in alphabetical order:

This concludes part 1. Would love to hear your feedback and thoughts. I’ll get part 2 out soon(ish).

As always, thanks for reading. Please hit the heart at the top of the email so more people can find us, share the post, and/or if you really really love me, pay $5/month or $50/year to get all the same stuff you get for free now.